The digital asset market is currently witnessing a profound behavioral divergence as a specific cohort of investors begins to pivot toward high-risk altcoins despite a backdrop of broader market exhaustion and declining trading volumes. While mainstream sentiment remains tethered to a narrative of stagnation and disappointment, recent on-chain data and exchange metrics suggest that a calculated repositioning is underway within the "OTHERS" category of the cryptocurrency ecosystem. This segment, which excludes the market’s five most dominant assets—Bitcoin (BTC), Ethereum (ETH), Solana (SOL), XRP, and BNB—is experiencing a localized surge in activity that contrasts sharply with the sluggish performance of the primary market leaders.

This development comes at a critical juncture for the industry. For much of the past year, the "altcoin season" that many retail participants anticipated has failed to materialize in a meaningful way. Instead, liquidity has remained concentrated in Bitcoin, bolstered by the success of spot ETFs and a "flight to quality" among institutional players. However, the latest analysis from CryptoQuant indicates that the tide may be turning beneath the surface. The divergence between falling overall market volume and rising specific altcoin volume suggests that the participants remaining in the market are no longer acting out of impulse or retail euphoria, but are instead executing deliberate, long-term accumulation strategies.

The Anatomy of the Volume Divergence

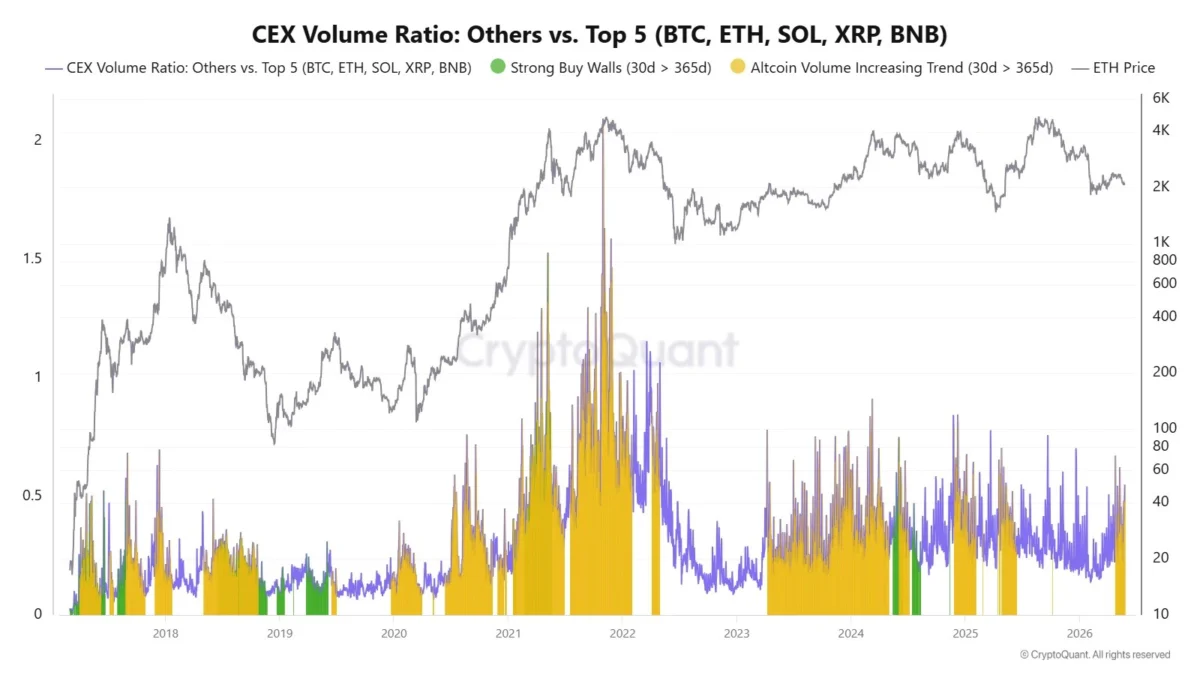

To understand the significance of the current trend, one must look at the specific composition of exchange volume. Traditionally, a healthy bull market is characterized by rising volumes across all sectors. Conversely, a bear market or a consolidation phase usually sees a uniform drop in participation. The current environment is anomalous because it fits neither of these descriptions perfectly. While total crypto trading volume has been on a steady decline since the failed recovery attempt in February, the volume ratio for smaller-cap altcoins has begun to climb.

This concentration of activity into the "OTHERS" group is a signal that professional traders and "smart money" entities are likely hunting for value in oversold assets that have been neglected during the Bitcoin-heavy phase of the cycle. By excluding the top five assets, analysts are able to filter out the noise of institutional Bitcoin flows and the high-frequency trading associated with dominant platforms like Solana and Ethereum. What remains is a raw look at the speculative appetite for the broader altcoin market—a segment that has been under intense selling pressure for nearly two years.

Market analysts note that when volume rises in a quiet market, it is rarely the result of retail "FOMO" (fear of missing out). Instead, it often represents the "absorption" phase of a market cycle, where large orders are filled slowly over time to avoid spiking the price. This behavior suggests that the current participants have a high degree of conviction that the bottom for these assets is either in or very close.

Historical Context: The Long Road to Stabilization

The current market structure is the result of a multi-year trend that began shortly after the 2021 market peak. Throughout 2022 and 2023, the altcoin market faced a series of systemic shocks, ranging from the collapse of the Terra ecosystem to the bankruptcy of major exchanges and lenders. These events decimated retail confidence and led to a "purge" of speculative capital.

By 2024, the introduction of spot Bitcoin ETFs in the United States further skewed the market dynamics. Capital that might have previously flowed into Ethereum or high-beta altcoins was instead diverted into regulated Bitcoin products. This led to a period of "Bitcoin Dominance" that pushed many altcoin-to-Bitcoin (ALT/BTC) ratios to multi-year lows. The OTHERS/BTC index, which tracks the total market cap of all cryptocurrencies excluding the top ten relative to Bitcoin, reflects this struggle. It has spent the better part of the last 24 months in a consistent downtrend, characterized by lower highs and lower lows.

However, the chronology of the last six months shows a shift from aggressive selling to a period of "basing." After the volatility of early 2025, the OTHERS/BTC ratio has begun to move sideways near the 0.12 level. In technical analysis, this transition from a vertical decline to horizontal movement is often the first prerequisite for a trend reversal. While the index remains below its 50-week, 100-week, and 200-week moving averages, the "momentum of the decline" has demonstrably slowed.

Technical Analysis: The Battle for the 50-Week Moving Average

The technical outlook for the broader altcoin market remains a study in patience. The OTHERS/BTC chart on TradingView highlights a persistent struggle against structural resistance. Despite the stabilization at the 0.12 support level, the market has yet to reclaim the 50-week moving average (MA). This specific moving average often acts as the "line in the sand" between a bear market and a nascent bull trend for altcoins.

Currently, the 50-week MA is trending downward, acting as a dynamic ceiling for price action. However, the recent increase in volume during minor recovery attempts suggests that there is enough buying pressure to potentially challenge this level in the coming months. If the OTHERS/BTC ratio can successfully reclaim the 50-week MA and hold it as support, it would represent a significant structural shift that hasn’t been seen since the early stages of the 2021 bull run.

Furthermore, the "accumulation" seen in the volume data is starting to show up in the form of "higher lows" on shorter timeframes. While the macro view is still one of caution, the micro view shows a market that is no longer reacting to negative news with the same level of panic that defined 2023. This "resilience" is a hallmark of a market that has been thoroughly de-leveraged.

Macroeconomic Factors and Institutional Influence

The divergence in altcoin volume cannot be viewed in a vacuum; it is heavily influenced by the global macroeconomic environment. For much of the last two years, the Federal Reserve’s "higher for longer" interest rate policy has acted as a headwind for risk assets. When "risk-free" yields on Treasury bonds are high, the incentive to speculate on volatile altcoins is diminished.

However, as inflation data begins to stabilize and the narrative shifts toward potential rate cuts or a "soft landing," the appetite for risk is slowly returning. Sophisticated investors are likely anticipating a shift in global liquidity. Historically, altcoins perform best when the US Dollar Index (DXY) weakens and global M2 money supply expands.

Additionally, the institutionalization of the space is starting to trickle down. While Bitcoin was the primary beneficiary of the first wave of institutional capital, there is growing interest in the underlying utility of the "OTHERS" category—specifically in sectors like Decentralized Physical Infrastructure Networks (DePIN), Artificial Intelligence (AI) integration, and Real-World Asset (RWA) tokenization. The rising volume in these specific sub-sectors suggests that investors are moving away from "meme-based" speculation and toward "thesis-driven" investing.

Market Sentiment: From Exhaustion to Disbelief

The psychological state of the current market is perhaps the most compelling indicator of a potential shift. Sentiment surveys and social media analytics show a prevailing sense of "exhaustion." Many retail investors who entered the market in 2021 have either exited at a loss or have become "passive holders" who are no longer actively trading.

In the Wall Street Cheat Sheet "Psychology of a Market Cycle," this phase is often labeled as "Depression" or "Disbelief." It is a period where the market moves sideways or slightly up, but the majority of participants remain skeptical, believing that any rally is simply a "dead cat bounce."

The CryptoQuant data suggests we are firmly in this disbelief phase. The fact that volume is rising while sentiment remains negative is a classic contrarian signal. It indicates that the "weak hands" have already been shaken out, and the current volume is being driven by "strong hands" who are comfortable buying into the apathy.

Implications for the Remainder of the Cycle

If the trend identified by CryptoQuant continues, the implications for the broader cryptocurrency market are significant. A sustained increase in altcoin volume, coupled with a breakout in the OTHERS/BTC ratio, would signal the start of a genuine capital rotation.

In previous cycles, capital has followed a predictable path: Bitcoin leads the way, followed by large-cap assets like Ethereum and Solana, and finally, liquidity trickles down into the mid-cap and small-cap "OTHERS" category. We have already seen the Bitcoin and large-cap phases play out to varying degrees. The current stabilization of the OTHERS/BTC ratio suggests that the market is preparing for the final stage of this rotation.

However, investors should remain aware of the risks. The structural weakness of the altcoin market means that any significant downturn in Bitcoin’s price would likely lead to a sharper decline in smaller assets. The "stabilization" at 0.12 is a support level, not a guarantee of a bounce. A breach of this level could lead to a final "capitulation" event before a true recovery can begin.

Conclusion: A Market in Transition

The digital asset landscape is currently a tale of two markets. On the surface, there is a sense of stagnation and a lack of clear direction as Bitcoin consolidates its gains. Beneath the surface, however, there is a hive of activity. The rising exchange volume for the "OTHERS" category, identified by CryptoQuant, serves as a testament to the enduring interest in the broader blockchain ecosystem.

This deliberate accumulation by a quiet cohort of investors suggests that the narrative of a "dead" altcoin market is premature. Instead, the market appears to be undergoing a necessary period of re-pricing and consolidation. As the OTHERS/BTC ratio attempts to find its footing after years of underperformance, the focus for observers should remain on the 50-week moving average and the continued persistence of this volume divergence. If these trends hold, the "quiet" phase of the market may soon give way to a period of renewed volatility and expansion, rewarding those who had the conviction to build positions when the rest of the market was looking elsewhere.