The digital asset landscape is currently navigating a period of profound structural transition, characterized by a stark divergence between surface-level sentiment and underlying transactional behavior. While the broader cryptocurrency market has been defined by months of sideways price action and a palpable sense of investor fatigue, recent data from on-chain analytics firm CryptoQuant reveals a specific anomaly: trading volume for "lower-tier" altcoins is rising even as overall market participation wanes. This trend, which focuses on assets outside the top five cryptocurrencies by market capitalization—Bitcoin (BTC), Ethereum (ETH), Solana (SOL), XRP, and BNB—suggests that a sophisticated cohort of market participants is actively positioning for a potential shift in market leadership.

The Anatomy of a Market Divergence

To understand the significance of the current shift, one must first examine the broader macroeconomic and psychological environment of the crypto industry. Following a brief period of optimism in early 2024, driven largely by the success of spot Bitcoin ETFs and the anticipation of the quadrennial halving event, the market entered a phase of protracted consolidation. This stagnation has led to a significant decline in aggregate trading volumes across major centralized exchanges (CEXs).

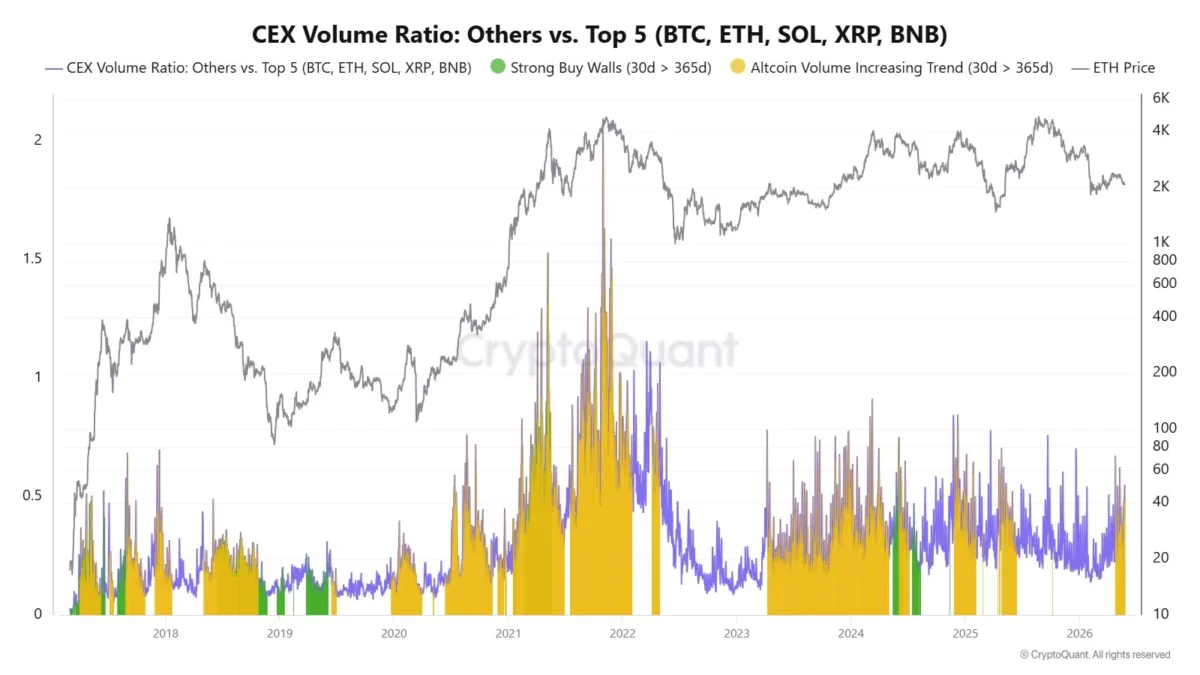

Standard retail sentiment, often measured by social media engagement and Google Search trends, has plummeted to multi-month lows. To the casual observer, the market appears dormant. However, the CryptoQuant data identifies a "behavioral divergence" that contradicts this narrative of inactivity. While the "Big Five" assets continue to see fluctuating or declining engagement, the category classified as "OTHERS"—representing the vast tail of mid-cap and small-cap altcoins—is experiencing a steady increase in exchange volume ratio.

This phenomenon is rarely accidental. In a high-volatility environment, rising volume during a period of price stagnation or slight decline often indicates accumulation by "strong hands"—institutional players, venture funds, or high-net-worth individuals who operate on longer time horizons than the average retail speculator. These participants appear to be absorbing the sell-side pressure from exhausted retail holders, building positions in projects they believe are undervalued relative to their technological or ecosystem growth.

Historical Context and the Altcoin Cycle

The current market structure bears a striking resemblance to the "pre-expansion" phases of previous market cycles, most notably the late 2020 period preceding the 2021 bull run. Historically, capital flows in the cryptocurrency market follow a predictable waterfall effect: capital first flows into Bitcoin, then moves to large-cap assets like Ethereum and Solana, and finally trickles down into the broader altcoin sector.

Throughout 2024 and the early stages of 2025, this waterfall effect appeared to be blocked. Bitcoin dominance remained stubbornly high, hovering between 50% and 60% of the total market share. This was largely due to the institutional nature of the current cycle, where capital entering through ETFs remained "locked" within the Bitcoin ecosystem rather than rotating into riskier assets.

However, the rising volume in the "OTHERS" category suggests that the rotation mechanism may finally be reactivating. The participants generating this volume are making deliberate, non-reactive decisions. Unlike the FOMO-driven (Fear Of Missing Out) volume seen at market peaks, this "quiet" volume is building session by session, often without accompanying price spikes that would alert the broader public. This suggests a strategic entry into the market, aimed at minimizing slippage and maintaining a low profile.

Analyzing the OTHERS/BTC Ratio and Technical Stabilization

A critical metric for assessing the health of the altcoin market is the OTHERS/BTC ratio. This index tracks the total market capitalization of all cryptocurrencies excluding the top 10 assets, measured against the price of Bitcoin. For more than two years, this ratio has been in a persistent downtrend, reflecting the extreme underperformance of altcoins relative to the market leader.

Technically, the OTHERS/BTC chart remains in a precarious position, but there are emerging signs of a structural "bottoming" process. The aggressive sell-offs that characterized the middle of 2024 have transitioned into a prolonged sideways consolidation phase, specifically around the 0.12 region.

Key technical indicators currently being monitored by analysts include:

- Moving Average Resistance: The ratio is currently trading below its 50-week, 100-week, and 200-week moving averages. For a confirmed trend reversal, the index would need to reclaim the 50-week moving average, which has acted as a formidable ceiling for several months.

- Momentum Deterioration: While the price ratio has not yet surged, the velocity of the decline has slowed significantly. This "momentum exhaustion" often precedes a change in trend direction.

- Volume Confirmation: Recent attempts to recover the 0.12 level have been accompanied by the rising volume spikes noted by CryptoQuant. This suggests that there is sufficient "buy-side" demand to defend this support zone, even if it hasn’t yet been enough to trigger a breakout.

If the OTHERS/BTC ratio manages to establish a series of higher highs and higher lows from this base, it would provide the first macro-level confirmation of an "altcoin season" since the 2021 peak.

The Role of Macroeconomic Factors

The divergence in altcoin volume cannot be viewed in a vacuum; it is heavily influenced by the global macroeconomic backdrop. As central banks, including the U.S. Federal Reserve, signal potential shifts in monetary policy, investors are beginning to re-evaluate their risk-on allocations.

In a high-interest-rate environment, capital tends to stay in "safe" assets like Bitcoin or U.S. Treasuries. However, as the market begins to price in liquidity injections and interest rate cuts, the search for "alpha" (excess returns) intensifies. This search naturally leads investors toward the altcoin sector, where smaller market caps allow for more significant percentage gains.

Furthermore, the maturation of specific sub-sectors within the altcoin market—such as Artificial Intelligence (AI), Real-World Asset (RWA) tokenization, and Decentralized Physical Infrastructure Networks (DePIN)—has provided fundamental reasons for this volume increase. Unlike previous cycles driven by pure speculation, there is a growing segment of the market focusing on projects with tangible utility and revenue-generating models.

Expert Perspectives and Market Sentiment

Market analysts at CryptoQuant suggest that the current "quiet" accumulation is a hallmark of a sophisticated market. "When you see volume increasing while sentiment remains negative, you are looking at a transfer of wealth," noted one senior analyst in a recent briefing. "Retail investors are selling because they are bored or frustrated by the lack of immediate gains, while institutional-grade participants are buying because they see a long-term value proposition."

The consensus among many industry experts is that the "Altcoin Season" of this cycle will look fundamentally different from those of the past. Rather than a "rising tide lifts all boats" scenario, analysts expect a more fragmented market where only projects with strong fundamentals and genuine adoption see significant appreciation. The rising volume in the "OTHERS" category likely reflects this selective accumulation, as traders pick winners based on data rather than hype.

Chronology of the Current Market Phase

To contextualize where the market stands, a timeline of the recent cycle is essential:

- February 2024: A sharp recovery attempt led by Bitcoin ETFs briefly lifted altcoin sentiment, but the rally failed to achieve broad-based sustainability.

- Q2 2024: Bitcoin dominance surged as altcoins faced heavy selling pressure, with many losing 50% or more of their value from the February highs.

- Q3 – Q4 2024: The market entered a "stagnation phase." Aggregate volumes dropped, and the OTHERS/BTC ratio hit multi-year lows.

- Early 2025: While prices remained flat, the CryptoQuant "volume divergence" began to appear. This marked the start of the current "silent accumulation" period.

- Current State: The market is testing the 0.12 support level on the OTHERS/BTC ratio, with volume continuing to climb despite the absence of a price breakout.

Broader Implications and Outlook

The implications of this data are significant for the remainder of the current market cycle. If the rising volume in the altcoin sector eventually leads to a price breakout, it would signal a major shift in capital concentration. For years, the market has been "top-heavy," with Bitcoin and a few select assets capturing the lion’s share of liquidity. A successful rotation into the "OTHERS" category would democratize liquidity across the broader ecosystem, potentially fueling innovation and development in smaller protocols.

However, risks remain. The technical structure of the altcoin market is still "structurally weak" on a macro basis. Until the OTHERS/BTC ratio can clear its long-term moving averages, the possibility of a "fakeout"—where volume rises but fails to result in a trend change—remains high. Additionally, any sudden volatility in the global financial markets or unexpected regulatory hurdles could derail this nascent accumulation phase.

In conclusion, the cryptocurrency market is currently a tale of two realities. On the surface, there is stagnation, exhaustion, and a lack of clear direction. Beneath the surface, however, the data reveals a calculated and persistent interest in the altcoin sector. For those monitoring the charts, the rising volume in "OTHERS" is a signal that the market’s internal mechanics are shifting. Whether this results in a full-scale altcoin season or a more localized rally for specific sectors, the "quiet" building of positions suggests that the next phase of the cycle may be closer than the current sentiment suggests.