The Technical Shift: From Mining to Staking

For seven years, Ethereum functioned as the primary ecosystem for Graphics Processing Unit (GPU) miners. Unlike Bitcoin, which relies on specialized Application-Specific Integrated Circuits (ASICs), Ethereum’s Ethash algorithm was designed to be "ASIC-resistant," allowing hobbyists and professionals alike to secure the network using consumer-grade hardware from manufacturers like NVIDIA and AMD. At its peak, the Ethereum network commanded a hashrate exceeding 900 Terahashes per second (TH/s), representing millions of individual GPUs worldwide.

On September 15, 2022, the Ethereum mainnet merged with the Beacon Chain, a PoS coordination layer. This move eliminated the need for energy-intensive mining, replacing miners with validators who "stake" ETH to propose and attest to new blocks. While the transition was a success for the Ethereum network’s energy efficiency—reducing its carbon footprint by more than 99.9%—it left a massive global infrastructure of mining hardware without its primary source of revenue.

The Great Migration and the Hashrate Flood

Immediately following the Merge, miners were faced with a binary choice: liquidate their hardware or point their hashing power toward alternative PoW blockchains. The primary recipients of this displaced hashrate included Ethereum Classic (ETC), Ravencoin (RVN), Ergo (ERG), and Flux (FLUX).

However, the sheer scale of Ethereum’s former mining community dwarfed these smaller networks. Before the Merge, Ethereum Classic had a hashrate hovering around 60 TH/s. Within 48 hours of the transition, that figure surged by over 280%, at one point crossing 300 TH/s as miners desperately sought a new "home" for their rigs.

In the world of PoW mining, network difficulty is a self-adjusting mechanism. As more hashrate joins a network, the difficulty of solving a block increases to ensure that block production remains constant. When hundreds of terahashes flooded into networks with significantly lower market capitalizations and lower block rewards than Ethereum, the difficulty spiked to unprecedented levels. The result was a mathematical inevitability: the "pie" of rewards remained the same size, but the number of people trying to claim a slice increased tenfold, leading to a drastic reduction in individual earnings.

The Economics of Negative Profitability

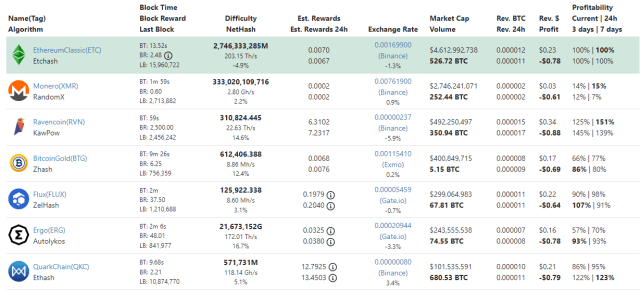

Data from mining calculators, including industry-standard platforms like WhatToMine, paints a grim picture for the current state of GPU mining. As of the latest reporting, none of the top-tier PoW cryptocurrencies are offering positive returns for the average miner when electricity costs are factored into the equation.

For example, Ethereum Classic (ETC), currently the most popular alternative for GPU miners, shows a net profit of approximately -$0.78 per hour for a rig utilizing three AMD RX 480 graphics cards. This calculation assumes an average residential electricity price of $0.10 per kilowatt-hour (kWh). Even for miners equipped with the most powerful consumer hardware available, such as the NVIDIA GeForce RTX 3090 Ti, hourly profits remain in the negative at roughly -$0.50.

The "breakeven" point for these miners has vanished. In many regions, particularly in Europe and parts of North America where energy prices have surged due to geopolitical instability, the cost of the electricity required to run the fans and processors of a mining rig far exceeds the market value of the coins being produced. This has led to the phenomenon of "mining at a loss," which some miners endure in the hope that the value of the mined coins will skyrocket in the future—a strategy often referred to as "speculative mining."

Market Impact: The GPU Secondary Market and Manufacturer Woes

The collapse of mining profitability has sent shockwaves through the hardware industry. During the 2020-2021 bull run, GPUs were notoriously difficult to find, with scalpers and miners driving prices to 200% or 300% of the Manufacturer’s Suggested Retail Price (MSRP).

With the Merge effectively killing the revenue stream for these devices, the secondary market is now being flooded with used hardware. Platforms like eBay and Craigslist have seen a massive uptick in listings for "lightly used" RTX 30-series and RX 6000-series cards. This sudden increase in supply has caused prices to plummet, benefiting gamers and workstation builders but hurting the resale value for former miners.

NVIDIA and AMD, the two dominant forces in the GPU space, have also had to adjust their financial outlooks. In recent earnings calls, both companies acknowledged a significant drop in demand for gaming GPUs as the mining "gold rush" ended. NVIDIA, in particular, had previously introduced "Lite Hash Rate" (LHR) versions of its cards to deter miners, but with the transition to PoS, the distinction between LHR and non-LHR hardware has become irrelevant to the broader market.

Industry Reactions and the Fate of Mining Pools

Major mining pools, which acted as intermediaries for thousands of individual miners, have been forced to pivot their business models. Ethermine, which was once the largest Ethereum mining pool in the world, announced the termination of its PoW mining services for ETH following the Merge. Instead of supporting alternative PoW coins, the organization transitioned to offering an "Ethereum Staking Service," allowing its user base to earn rewards through the new PoS system.

Other pools have attempted to support "merged mining" or "auto-switching" algorithms that move a miner’s hashrate to the most profitable coin at any given moment. However, when the entire market is unprofitable, these tools offer little relief.

Vitalik Buterin, the co-founder of Ethereum, has long maintained that the move to PoS was necessary for the long-term scalability and sustainability of the network. In various public forums, Buterin suggested that miners who wished to continue their craft should move to Ethereum Classic, noting that ETC has a "welcoming community" for PoW proponents. While the community may be welcoming, the current economic reality suggests that the ETC network simply cannot provide a livelihood for the millions of miners displaced by its parent chain.

Broader Implications and the Future of Proof-of-Work

The current crisis in GPU mining raises existential questions about the future of PoW consensus for any asset other than Bitcoin. Bitcoin remains insulated from this specific crisis because it utilizes SHA-256 ASIC miners, which are incompatible with the algorithms used by Ethereum or its GPU-based alternatives.

For "Alt-PoW" coins to become profitable again, one of two things must happen:

- Price Appreciation: The market value of coins like ETC, RVN, or ERG must increase significantly to offset the high difficulty and electricity costs.

- Miner Capitulation: A vast majority of miners must turn off their machines, causing the network difficulty to drop until the remaining miners can once again achieve profitability.

As of late September 2022, the market is in a state of "wait and see." Ether’s price has remained volatile, currently floating around the $1,400 mark, down roughly 6% over the past week as the "buy the rumor, sell the news" sentiment took hold post-Merge. The broader macroeconomic environment, characterized by high inflation and rising interest rates, further complicates the recovery of the crypto mining sector.

While some industry analysts speculate that a new "King of GPU Mining" could emerge in the next bull cycle, the current data suggests that for the average hobbyist, the era of "printing money" with a home computer has come to a definitive end. The infrastructure that once secured the world’s second-largest blockchain is now either collecting dust, being sold for parts, or running at a loss, marking a somber conclusion to the most lucrative chapter in the history of decentralized computing.