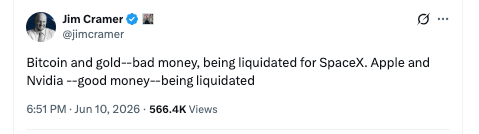

In a recent and characteristically blunt assessment, prominent financial commentator Jim Cramer has declared that "bad money" is being liquidated from both Bitcoin and gold to fund the highly anticipated Initial Public Offering (IPO) of SpaceX, valued at an estimated $75 billion. Cramer, the host of CNBC’s "Mad Money," articulated this viewpoint through a post on the social media platform X (formerly Twitter), sparking a predictable flurry of reactions from the cryptocurrency and precious metals communities. His assessment draws a stark contrast between assets he deems unproductive and those he views as generating valuable cash flow, particularly in the context of significant upcoming corporate events.

The core of Cramer’s argument rests on his categorization of assets as either "good money" or "bad money." He defines "good money" as capital derived from high-quality, income-producing assets. In the context of the SpaceX IPO, Cramer specifically pointed to shares of companies like Apple and, by implication, Nvidia, as examples of "good money" that investors are likely reallocating. Conversely, "bad money," according to Cramer’s definition, represents assets that have become a "sunk cost" – requiring continuous liquidity injections without generating commensurate returns. It is this category, he asserts, that Bitcoin and gold currently fall into, with investors reportedly divesting from these assets to capitalize on the lucrative opportunity presented by the SpaceX IPO.

This latest pronouncement from Cramer is not an isolated incident but rather the continuation of a long and often volatile public discourse he has had with both Bitcoin and gold. His commentary on digital assets, in particular, has been subject to significant shifts over time, leading many observers to characterize his stance as inconsistent. For instance, earlier in the year, Cramer had speculated on the possibility of the U.S. government, under a potential Donald Trump administration, purchasing Bitcoin for the nation’s strategic reserve, even suggesting a price point of $60,000. This prediction was made when Bitcoin was trading above $60,000, a level it has since revisited, but no such government acquisition has materialized.

Furthermore, historical commentary from Cramer reveals a period where he expressed considerable optimism about Bitcoin, at one point even declaring it superior to gold. He had also stated that his personal investment returns from digital currencies had surpassed those from traditional assets like gold and stocks. These pronouncements were made during periods of significant market exuberance, reflecting the prevailing bullish sentiment. However, as the market has transitioned from a bull run to a more challenging price pullback, Cramer’s tone has demonstrably shifted. His current labeling of both Bitcoin and gold as "bad money," despite his past self-identification as a "gold bug," underscores this dramatic change in perspective.

The Rationale Behind "Bad Money" Designation

Cramer’s distinction between "good" and "bad" money, while perhaps simplistic to some, attempts to encapsulate a fundamental investment principle: the efficiency of capital allocation. "Good money," in his framework, is money that is working for the investor, generating tangible returns and appreciating in value. Assets like established tech giants such as Apple, and high-growth companies like Nvidia, are often seen as exemplars of this due to their consistent revenue streams, profitability, and potential for capital appreciation. Investors might liquidate other holdings to invest in these companies, especially when they are perceived as poised for significant gains, such as through an IPO.

The concept of "bad money" as a sunk cost highlights a common behavioral trap in investing. This refers to an asset that has depreciated significantly or has failed to meet performance expectations, yet investors continue to hold onto it, often hoping for a recovery. The persistence in holding such assets can tie up capital that could be more productively deployed elsewhere. Cramer’s assertion suggests that he views Bitcoin and gold, in their current market performance, as fitting this description. Investors, in his view, are recognizing the lack of immediate positive returns from these assets and are choosing to redirect their funds towards more promising opportunities like the SpaceX IPO.

The SpaceX IPO itself represents a monumental event in the financial world. The private space exploration company, founded by Elon Musk, has achieved remarkable milestones in space travel and is poised to enter the public markets, offering a rare opportunity for investors to gain exposure to its innovative technologies and ambitious vision. The sheer scale of the potential $75 billion valuation indicates immense investor interest and a significant influx of capital seeking to participate in this transformative venture.

A History of Volatile Takes on Bitcoin

Jim Cramer’s relationship with Bitcoin has been a subject of considerable debate and scrutiny within the crypto community. His public pronouncements have often been perceived as capricious, leading to accusations of employing "rage bait" tactics to generate engagement on social media platforms. This strategy, critics argue, aims to provoke strong emotional responses, thereby increasing visibility and influence.

His flip-flopping on Bitcoin is well-documented. At one point, he was a vocal proponent, even predicting a scenario where the U.S. government would acquire Bitcoin for its strategic reserves. This was a significant endorsement, coming from a mainstream financial figure. However, as market conditions shifted and Bitcoin experienced price corrections, his narrative evolved. The contrast between his past bullish statements and his current bearish assessment highlights the dynamic nature of market sentiment and the challenges of forecasting asset performance, particularly for volatile assets like cryptocurrencies.

His earlier praise for Bitcoin often coincided with periods of strong market performance, where the digital asset was experiencing significant price appreciation. During these times, Cramer’s commentary reflected the prevailing optimism, emphasizing Bitcoin’s potential and its advantages over traditional assets. Conversely, his current criticisms align with a period of market downturn, where investors are reassessing their portfolios and seeking more stable or higher-growth opportunities. This pattern suggests that Cramer’s public stance may be heavily influenced by short-term market trends, a characteristic that has drawn criticism from those who advocate for a more long-term investment perspective.

Reactions from the Crypto and Gold Communities

Cramer’s recent "bad money" declaration regarding Bitcoin and gold was met with swift and often humorous responses from users on X. The cryptocurrency and precious metals communities have a history of pushing back against Cramer’s commentary, viewing it as either misinformed or deliberately provocative.

A recurring theme in the responses is the notion that when Cramer turns negative on an asset, it signals that the market has reached a bottom. This contrarian indicator, often referred to as the "Cramer Bottom," suggests that his bearish pronouncements might inadvertently signal an opportune moment for investors to consider buying, as the sentiment he expresses may be indicative of peak pessimism.

One user on X, @BigRyan, humorously suggested that Cramer’s negative take on Bitcoin might actually be a positive sign. The implication is that once a prominent critic like Cramer abandons an asset, it signifies that the asset has likely seen its worst performance and is poised for a recovery. This sentiment is a testament to the contrarian investment strategies that have emerged within the crypto space, often in direct response to mainstream financial commentary.

Another user, @realpeteyb123, offered a more direct and succinct quip, questioning the source of Cramer’s information and suggesting that his pronouncements might be misguided. This highlights a broader skepticism towards traditional financial media’s understanding of decentralized assets and their underlying value propositions.

Broader Implications and Market Dynamics

Cramer’s commentary, while often polarizing, does tap into broader market dynamics that influence asset allocation decisions. The anticipation of a major IPO like SpaceX’s can indeed create a significant gravitational pull for capital. Investors, ranging from institutional players to retail traders, often rebalance their portfolios to participate in such high-profile offerings. This can lead to outflows from other asset classes, particularly those perceived as less promising in the short to medium term.

The classification of Bitcoin and gold as "bad money" by Cramer, however, warrants further examination beyond his specific commentary. Bitcoin, often hailed as "digital gold," is frequently positioned as a hedge against inflation and a store of value, similar to traditional gold. Both assets have experienced periods of volatility, influenced by macroeconomic factors, investor sentiment, and regulatory developments.

Gold, for centuries, has been considered a safe-haven asset, sought after during times of economic uncertainty and geopolitical instability. Its performance is often inversely correlated with the strength of the U.S. dollar and interest rates. In recent times, while gold has seen periods of appreciation, it has also faced challenges from competing asset classes and shifts in global economic conditions.

Bitcoin, as a relatively newer asset class, exhibits a higher degree of volatility. Its price movements are influenced by a complex interplay of technological developments, adoption rates, regulatory clarity, and speculative trading. The narrative around Bitcoin as a hedge against inflation or a digital store of value is still evolving, and its correlation with traditional markets, including equities, has been observed to fluctuate.

The SpaceX IPO represents a unique opportunity for investors to participate in the growth of a company at the forefront of technological innovation in the aerospace sector. Companies like SpaceX are at the vanguard of disruptive industries, attracting significant investment interest due to their potential for high growth and long-term impact. The capital required to fund such ventures, and the desire of investors to capitalize on their potential, can lead to a reallocation of funds from other investments.

Cramer’s assertion, therefore, can be interpreted as a commentary on investor behavior and the perceived attractiveness of different investment opportunities. When a highly anticipated event like the SpaceX IPO emerges, it inevitably forces investors to make choices about where to deploy their capital. His categorization of Bitcoin and gold as "bad money" in this context suggests that, in his view, these assets are currently not offering the same level of compelling return potential as the opportunity presented by SpaceX’s public debut.

Ultimately, the ongoing debate surrounding Cramer’s pronouncements highlights the diverse perspectives and strategies within the financial markets. While some may dismiss his commentary as mere noise, others may find value in his contrarian signals or use his assessments as a starting point for their own due diligence. The dynamic interplay between established financial commentators, evolving asset classes like Bitcoin, and significant corporate events like the SpaceX IPO will continue to shape investment narratives and influence market sentiment. The true performance of Bitcoin, gold, and the assets Cramer deems "good money" will ultimately be determined by their ability to deliver value and returns to investors over the long term.