The digital asset market is currently navigating a complex period of transition characterized by a stark divergence between visible price action and underlying liquidity flows. While the broader cryptocurrency environment remains clouded by months of persistent selling pressure and a prevailing sense of investor exhaustion, new on-chain data suggests that a strategic shift is occurring within the altcoin sector. According to recent analytics provided by CryptoQuant, a specific behavioral anomaly has emerged: while overall market enthusiasm and trading volumes are declining, exchange volume for a specific subset of altcoins is quietly rising. This trend indicates that while the casual retail participant may be disengaging, a more deliberate cohort of investors is actively positioning themselves for a potential shift in market leadership.

The macro environment framing this signal is one of cautious stagnation. For much of the first half of the year, crypto trading volumes across major centralized exchanges (CEXs) have been on a downward trajectory. Following a brief period of optimism during a February recovery attempt, investor sentiment has drifted into negative territory, exacerbated by weeks of sideways price movement and various macroeconomic headwinds, including fluctuating interest rate expectations and regulatory uncertainty. To the average observer, the market feels listless; however, the CryptoQuant data identifies a "behavioral divergence" beneath the surface that suggests the altcoin sector is far from dead.

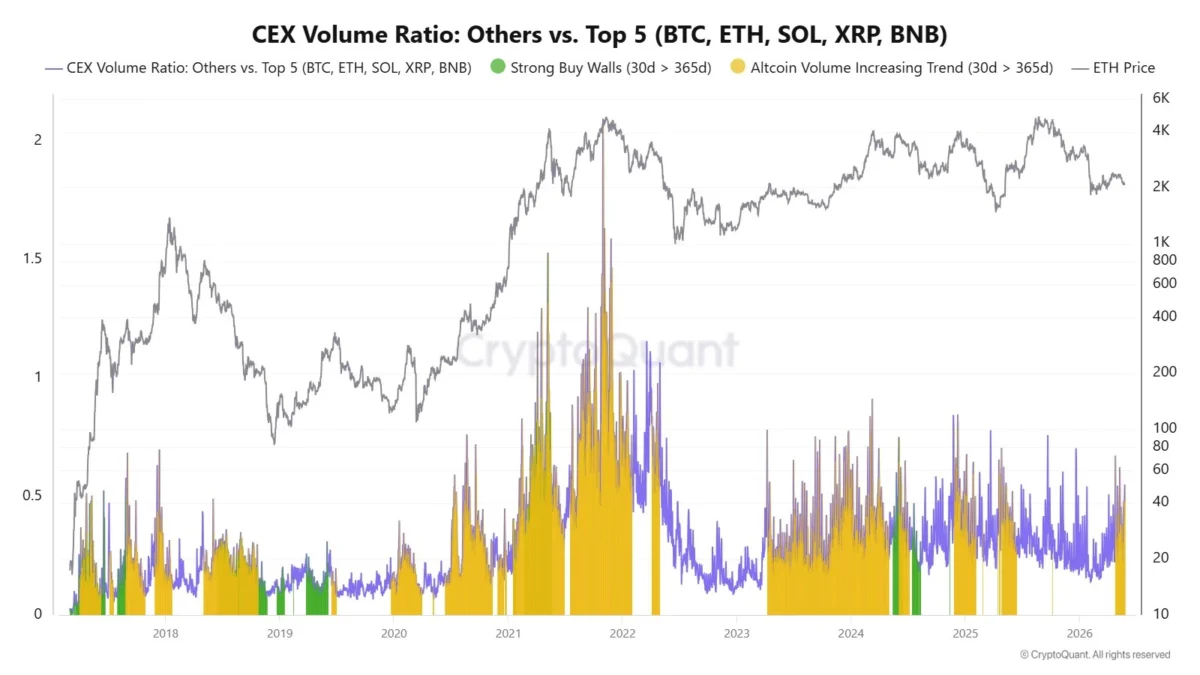

The Anatomy of the Volume Divergence

The core of the current market signal lies in the exchange volume ratio of "OTHERS" versus the top five crypto assets. In this context, the top five assets—Bitcoin (BTC), Ethereum (ETH), Solana (SOL), XRP, and BNB—represent the established market leaders that often capture the lion’s share of institutional and retail attention. These assets typically move in high correlation with the broader market and are often viewed as the "blue chips" of the digital asset space.

The "OTHERS" category, conversely, encompasses the vast landscape of mid-cap and small-cap altcoins. This segment is traditionally associated with higher speculative risk, higher volatility, and the potential for "alpha" or outsized returns during the early stages of a market cycle. The anomalous data point identified by CryptoQuant shows that while the total market volume is shrinking, the volume specifically attributed to these "OTHERS" is increasing.

This divergence is significant because it suggests a concentration of activity in the riskier, more speculative end of the market at a time when general participation is at a multi-month low. Historically, when volume rises in a quiet market, it is rarely the result of reactive or emotional trading. Instead, it often points toward "smart money" or disciplined accumulators who are building positions while liquidity is thin and competition for entries is low.

Historical Context and the OTHERS/BTC Ratio

To understand the implications of this volume spike, one must look at the long-term relationship between altcoins and Bitcoin. The OTHERS/BTC index, which tracks the total market capitalization of all cryptocurrencies excluding the top 10 assets relative to Bitcoin’s market cap, provides a clear visualization of this relationship. For more than two years, this ratio has been in a persistent downtrend, reflecting a period where capital has remained heavily concentrated in Bitcoin while altcoins struggled to maintain their value.

The 2024-2025 cycle has, thus far, been defined by "Bitcoin Exceptionalism." The approval of spot Bitcoin ETFs in the United States and the subsequent institutional inflow created a vacuum where Bitcoin outperformed the rest of the market by a wide margin. Many participants who positioned for a traditional "altcoin season"—a period where smaller assets outperform BTC—found themselves sidelined as the expected rotation failed to materialize with the same intensity seen in 2017 or 2021.

However, the technical structure of the OTHERS/BTC chart is now showing signs of stabilization. After an aggressive decline throughout 2024, the ratio has entered a prolonged sideways consolidation phase, specifically finding a floor near the 0.12 region. While the ratio remains below the critical 50-week, 100-week, and 200-week moving averages—confirming that Bitcoin still holds structural dominance—the slowing of downward momentum is a necessary precursor to a trend reversal. Major market rotations historically begin with this type of "base-building" behavior, where sellers become exhausted and buyers slowly begin to absorb the remaining supply.

A Chronology of Market Sentiment and Capital Flow

The path to the current state of the altcoin market can be traced through several distinct phases over the past eighteen months:

- The Q1 2024 Surge: Bitcoin led the market to new all-time highs, driven by ETF inflows. Altcoins saw a brief, high-intensity spike, particularly in the meme coin and Artificial Intelligence (AI) sectors, leading many to believe a full-scale altcoin season was imminent.

- The Q2-Q3 2024 Correction: As Bitcoin’s momentum stalled, altcoins suffered disproportionately. Many assets retraced 50% to 80% of their yearly gains, leading to widespread retail capitulation and a "washout" of leveraged positions.

- The Late 2024 Stagnation: The market entered a period of "boredom," where low volatility and declining volumes led to a drop in social media engagement and retail trading activity.

- The Early 2025 Divergence: The current phase, identified by CryptoQuant, where overall volume continues to fade, but internal metrics show a quiet, persistent accumulation of non-top-5 assets.

This chronology suggests that the market is currently in a "disbelief" phase. Most retail investors, having been burned by the mid-2024 correction, are skeptical of any upward movement in altcoins. This skepticism is visible in sentiment data, where "Fear and Greed" indices for altcoins often linger in the "Fear" or "Apathy" zones even when prices stabilize.

Institutional Influence and Ecosystem Growth

The shift toward altcoins is not merely a technical phenomenon; it is supported by fundamental developments within specific ecosystems. While the "top 5" assets are often the focus of headlines, the "OTHERS" category includes burgeoning sectors such as Decentralized Physical Infrastructure Networks (DePIN), Real-World Asset (RWA) tokenization, and advanced Layer-2 scaling solutions.

Industry analysts suggest that the rising volume in these sectors may be linked to venture capital (VC) firms and institutional "sleeper" funds that are mandated to deploy capital into infrastructure projects. Unlike the meme coin frenzies of previous years, the current accumulation appears to be focusing on projects with tangible utility and revenue-generating models. For instance, the expansion of Chainlink’s integration with traditional financial institutions and the growth of the Base ecosystem have provided fundamental reasons for investors to look beyond the top five assets.

Furthermore, the stabilization of the OTHERS/BTC ratio at 0.12 suggests that the market has found a valuation level where the risk-to-reward ratio for altcoins has become attractive to long-term holders. At these levels, the "downside risk" against Bitcoin is perceived to be lower than the potential "upside capture" should a rotation occur.

Implications for the Remainder of the Cycle

The continuation of this trend carries several implications for the broader crypto economy. If the volume divergence persists, it will likely lead to a "bottoming out" process for the altcoin market. However, a confirmed breakout requires more than just stabilization; it requires the OTHERS/BTC ratio to reclaim its 50-week moving average and establish a series of higher highs.

From a liquidity perspective, the market is waiting for a catalyst. This could come in the form of a shift in global macro liquidity—such as a more aggressive pivot by the Federal Reserve toward interest rate cuts—or a regulatory breakthrough that provides more clarity for decentralized finance (DeFi) protocols. When global liquidity (M2 money supply) increases, it typically flows down the "risk curve," starting with Bitcoin and eventually flooding into the altcoin sectors.

The current behavior of the "quiet cohort" identified by CryptoQuant suggests they are front-running this eventual return of liquidity. By accumulating during a period of disinterest, these participants are positioning themselves to benefit from the volatility that occurs when the broader market eventually "wakes up" and attempts to chase the new trend.

Conclusion: A Market in Transition

While the consensus view on the altcoin market remains one of skepticism and caution, the data provides a more nuanced narrative. The rise in exchange volume for the "OTHERS" segment, amidst a general decline in market participation, is a classic signature of a market reaching a structural turning point. It reflects a transition from "weak hands" to "strong hands," and from reactive selling to deliberate accumulation.

The road ahead for altcoins remains challenging, and the shadow of Bitcoin dominance still looms large. However, the stabilization of the OTHERS/BTC index and the persistent volume divergence suggest that the foundation for the next phase of the cycle is being laid now, in the quietest hours of the market. Investors and analysts alike will be watching the 0.12 support level and the 50-week moving average closely; a decisive move above these markers would signal that the "altcoin winter" has finally thawed, ushering in a period of renewed speculative vigor and ecosystem expansion.