The completion of the Ethereum Merge on September 15, 2022, marked one of the most significant technical milestones in the history of blockchain technology, but it simultaneously triggered a financial catastrophe for the global GPU mining industry. By transitioning from a Proof-of-Work (PoW) consensus mechanism to Proof-of-Stake (PoS), the Ethereum network effectively rendered an estimated $4 billion worth of mining hardware obsolete overnight. As thousands of miners scrambled to find alternative revenue streams, the resulting migration of hashrate into smaller PoW ecosystems has driven mining profitability into negative territory, signaling what many analysts describe as the "end of an era" for home-based and small-scale graphics card mining.

Before the Merge, Ethereum was the primary destination for GPU miners, accounting for over 90% of all GPU-based mining revenue. Its hashrate—a measure of the total computational power securing the network—regularly hovered between 800 and 900 Terahashes per second (TH/s). When the network successfully merged with the Beacon Chain, these miners were forced to either shut down their operations, sell their equipment, or point their "rigs" toward alternative PoW coins such as Ethereum Classic (ETC), Ravencoin (RVN), Ergo (ERG), and Flux. However, the sheer volume of Ethereum’s displaced hashrate was too massive for these smaller networks to absorb, leading to a "difficulty bomb" that has made mining these coins more expensive than the rewards they provide.

The Mechanics of the Profitability Collapse

To understand why mining profits have cratered, one must look at the relationship between hashrate and mining difficulty. In a PoW system, the network automatically adjusts its difficulty to ensure that blocks are found at a consistent interval, regardless of how much computational power is participating. When a massive influx of miners joins a small network, the difficulty spikes to prevent coins from being minted too quickly.

Before the Merge, Ethereum Classic (ETC) maintained a hashrate of approximately 25 to 30 TH/s. Within 24 hours of the Merge, that figure surged by nearly 500%, peaking at over 300 TH/s. Because the market value of ETC did not experience a corresponding 500% increase, the rewards distributed to each individual miner were diluted to the point of insolvency.

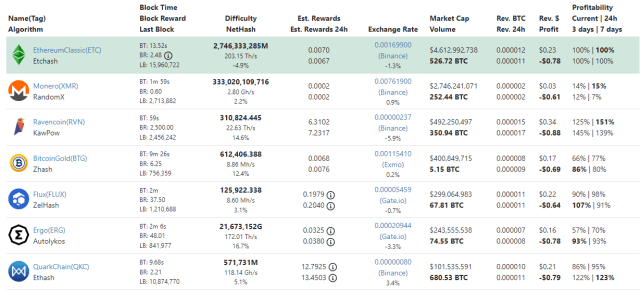

According to data from the mining profitability calculator WhatToMine, the economic reality for miners is now bleak. Utilizing a standard setup of three AMD Radeon RX 480 graphics cards—a once-profitable staple of the mining community—the net profit for mining Ethereum Classic has dropped to approximately -$0.78 per hour. This calculation assumes a baseline electricity cost of $0.10 per kilowatt-hour (kWh). Even for those utilizing top-of-the-line hardware, such as the NVIDIA GeForce RTX 3090 Ti, hourly profits remain in negative territory at roughly -$0.50. In this environment, miners are effectively paying their utility companies for the privilege of securing a blockchain, receiving tokens worth significantly less than the power consumed to generate them.

A Chronology of the Transition

The road to this profitability crisis was paved over several years, characterized by a series of high-stakes upgrades known as the Ethereum 2.0 roadmap.

- December 2020: The launch of the Beacon Chain introduced the Proof-of-Stake consensus layer, running in parallel with the main PoW chain. This allowed users to begin staking their ETH, though it did not yet process transactions.

- April 2021: The "Berlin" upgrade optimized gas prices and improved security, signaling the network’s readiness for more complex transitions.

- August 2021: The London Hard Fork introduced EIP-1559, which began burning a portion of transaction fees. This was the first major blow to miner revenue, as it reduced the "tips" miners received from users.

- June-August 2022: Final testnet merges on Ropsten, Sepolia, and Goerli were completed successfully, confirming that the "Merge" was imminent and technically sound.

- September 15, 2022: The Terminal Total Difficulty (TTD) was reached, and the execution layer merged with the consensus layer. Ethereum mining officially ceased at block 15,537,393.

The immediate aftermath saw a chaotic "migration of the masses." Within hours, the hashrates of Ravencoin and Ergo doubled and tripled, respectively. However, the market liquidity of these coins is a fraction of Ethereum’s. While Ethereum once supported billions in daily trading volume, coins like Ergo often see less than $10 million. This liquidity gap means that even if miners were to earn tokens, any mass selling to cover electricity bills would further suppress the price, creating a "death spiral" of profitability.

Industry Reactions and Market Sentiment

The mining industry’s reaction has been split between resignation and desperate pivot strategies. Major mining pools, which once managed the collective power of thousands of individuals, have been forced to adapt. Ethermine, formerly the world’s largest Ethereum mining pool, announced it would not support any PoW forks of Ethereum and instead launched a "staking-as-a-service" platform to align with the new PoS model.

In the hardware sector, the secondary market for GPUs has been flooded with used equipment. Sites like eBay and Craigslist have seen a massive uptick in listings for "lightly used" mining rigs as hobbyist miners attempt to recoup their capital investment before hardware prices drop further. This surplus of GPUs has also impacted manufacturers like NVIDIA and AMD, who are facing a decline in demand for new cards after two years of record-breaking sales driven by the mining boom.

Some industrial-scale miners have attempted to pivot to High-Performance Computing (HPC) or Artificial Intelligence (AI) data processing. These firms are repurposing their GPU clusters to provide cloud computing services, which offers a more stable revenue stream than the volatile crypto markets. However, this transition requires significant additional investment in infrastructure and networking, which is not an option for the average home miner.

Broader Implications and the Future of PoW

The collapse of GPU mining profitability raises fundamental questions about the future of Proof-of-Work outside of Bitcoin. Bitcoin remains secure because it uses Application-Specific Integrated Circuits (ASICs)—specialized hardware that cannot be used for anything other than mining Bitcoin. GPU-based coins, however, are now in a precarious position.

With mining being unprofitable, there is a risk that hashrates will eventually drop as miners turn off their machines to save money. A lower hashrate makes a network more vulnerable to a "51% attack," where a malicious actor gains control of the majority of the network’s computing power. If these alternative PoW chains cannot find a way to increase their market value or utility, they may face a slow decline in both security and relevance.

Furthermore, the environmental narrative has shifted. One of the primary drivers for the Ethereum Merge was the reduction of energy consumption by more than 99.9%. In a world increasingly focused on ESG (Environmental, Social, and Governance) standards, PoW coins that rely on GPU mining are finding it harder to attract institutional investment. The current "unprofitability" of mining acts as a natural, albeit painful, deterrent to high energy consumption.

Fact-Based Analysis of the Path Forward

For GPU mining to become viable again, one of two things must happen: either the market value of alternative PoW coins must increase by several hundred percent, or a significant portion of the global mining fleet must be permanently decommissioned to lower the network difficulty.

Currently, the "break-even" price for Ethereum Classic, given the current hashrate, would require the coin to trade well above $100—a far cry from its current valuation in the $20 range. Similarly, Ravencoin and Ergo would need unprecedented bull runs to support their current levels of computational competition.

In conclusion, the Ethereum Merge has fundamentally rewritten the economics of the cryptocurrency landscape. While the transition was a triumph for Ethereum’s scalability and environmental goals, it has left a trail of economic destruction in the mining sector. The "Great Migration" of miners to alternative chains has proven that hashrate follows profit, but without the massive ecosystem of Ethereum to support it, that hashrate has become its own worst enemy. For now, the era of "easy" GPU mining profits is over, leaving the industry to face a cold reality where electricity bills outpace digital rewards.