The global financial ecosystem is currently undergoing a structural transformation as traditional financial instruments—ranging from sovereign debt and corporate equities to physical commodities and real estate—are increasingly migrated onto blockchain infrastructure. This process, known as tokenization, involves creating digital representations of real-world assets (RWAs) that are issued, managed, and settled directly on distributed ledgers. According to recent data and market analysis, tokenized RWAs have moved beyond the experimental phase, approaching a total of $30 billion in assets under management (AUM). This surge represents a fundamental shift in the "rails" of global finance, offering 24/7 market access, near-instantaneous settlement, and a significant reduction in the costs associated with traditional intermediaries.

For decades, the back-end infrastructure of global finance has relied on a fragmented web of clearinghouses, custodians, and legacy settlement systems that often require several days to finalize transactions. The move toward blockchain-based rails addresses these inefficiencies by providing a unified, transparent ledger that serves as a single source of truth for all market participants. As institutional confidence grows, the strategic focus for major financial entities has shifted from a speculative curiosity about digital assets to a practical execution of on-chain integration.

The Regulatory Catalyst: The GENIUS Act and the 2025 Paradigm Shift

The acceleration of the RWA market can be traced back to a series of pivotal regulatory milestones that occurred throughout 2024 and 2025. Most notable was the passage of the GENIUS Act in July 2025, which established a comprehensive federal framework and standardized settlement infrastructure for payment stablecoins and digital representations of securities. Before this legislation, institutional participation was often hampered by a lack of legal clarity regarding the custody, reporting, and settlement of digital assets.

The GENIUS Act, alongside emerging mandates for on-chain capital markets, provided the necessary guardrails for large-scale capital entry. Updated compliance thresholds from the Office of the Comptroller of the Currency (OCC) and other regulatory bodies clarified how banks and financial institutions could safely custody digital assets. These developments effectively "opened the floodgates," allowing traditional asset managers to leverage the transparency of public ledgers. The ability to conduct real-time monitoring of asset flows and counterparty risk aligns perfectly with the strict risk management requirements of the institutional sector, creating a more resilient environment than the opaque systems of the past.

A Chronology of Growth: The Race to the $1 Billion Milestone

The evolution of the RWA market has not been uniform across all asset classes. While the overall market is trending toward $30 billion, the velocity of capital formation varies significantly between institutional-grade instruments and retail-focused assets. A key metric for assessing market maturity is the time it takes for a specific asset class to reach $1 billion in total on-chain valuation from its initial issuance.

Data reveals that institutional categories are scaling at an unprecedented pace. Asset-backed credit, for instance, achieved the $1 billion milestone in just 6.1 months. Specialty finance followed, reaching the mark in 21.5 months. In contrast, more retail-oriented sectors like tokenized commodities took 36.2 months to hit the $1 billion threshold, while tokenized stocks have yet to reach that level of scale.

This disparity highlights a critical trend: institutional capital is currently the primary driver of market expansion. While retail interest in "crypto-native" assets remains significant, the "heavy lifting" of embedding traditional financial instruments into blockchain infrastructure is being performed by large-scale entities. The rapid scaling of asset-backed credit suggests that when the technical and regulatory infrastructure is ready, institutional players are prepared to deploy capital in massive increments, rather than the gradual accumulation typically seen in retail markets.

Mapping the Asset Landscape: Treasuries, Commodities, and Managed Funds

Within the current $30 billion RWA ecosystem, specific asset classes have emerged as leaders in terms of liquidity and adoption. U.S. Treasury debt represents the largest single RWA asset class on-chain. This is epitomized by high-profile products such as BlackRock’s BUIDL (BlackRock USD Institutional Digital Liquidity Fund) and Circle’s USYC. These assets provide a low-risk entry point for investors seeking the yield of government debt combined with the operational efficiency of blockchain-based settlement.

On the consumer side, tokenized commodities remain the most popular category. Physical gold, in particular, has seen significant traction, with $40.5 billion in total tokenized gold volumes captured across various chains. The appeal of tokenized gold lies in its fractionalization and ease of transfer, allowing investors to hold and trade exposure to the precious metal without the logistical burdens of physical storage or the delays of traditional gold ETFs.

However, it is important to note that the valuation of certain RWAs remains complex. Aggregators such as rwa.xyz track tokens representing highly illiquid physical assets like real estate. Because these assets do not trade on continuous secondary markets, their present market value is often based on best-available estimates rather than real-time price discovery. As the market matures, the development of more robust secondary trading venues for these illiquid assets will be a critical step toward achieving true market transparency.

The New Onboarding Funnel: Institutions Leading the Charge

One of the most surprising findings in the recent shift toward RWAs is the change in how users enter the digital asset ecosystem. Historically, adoption followed a "retail-first" model, where individual investors entered through Bitcoin or Ethereum before exploring more complex decentralized finance (DeFi) applications. The RWA data suggests an inversion of this sequence.

Analysis of nearly 400,000 distinct RWA holding addresses indicates that RWAs are now acting as a "top-of-funnel" mechanism for institutional participants. On the Ethereum network—the largest hub for RWA activity—there has been an explosive growth in the number of wallets receiving RWA tokens within the first six months of their creation.

Institutional-grade assets like specialty finance and asset-backed credit are predominantly held by entirely new wallets. In many cases, these addresses receive their first RWA token within one week of the wallet’s creation. This suggests that these wallets are not belonging to existing crypto enthusiasts but are purpose-built, whitelisted addresses created by financial institutions specifically to manage these new digital instruments. This "purpose-built" behavior contrasts sharply with retail-leaning categories like tokenized stocks or commodities, where a significant portion of participation comes from legacy "crypto-native" wallets that have been active for years.

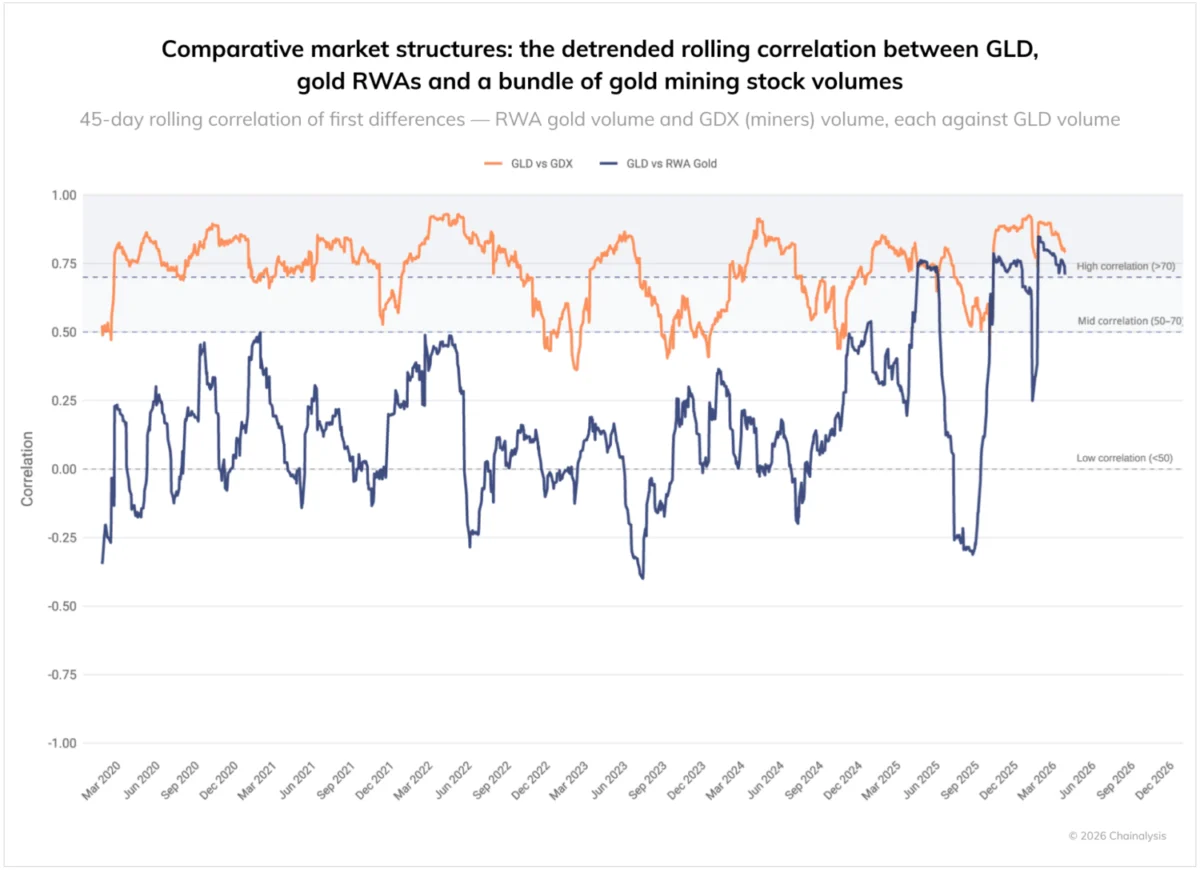

Market Maturation: When On-Chain Trading Mirrors TradFi

A critical test for the long-term viability of RWAs is whether tokenized assets behave like their traditional counterparts in the "real world." If a tokenized asset only moves in response to crypto market volatility, it fails to serve its purpose as a stable financial instrument.

Recent analysis of tokenized gold provides a promising case study in market maturation. Historically, the trade volume of tokenized gold showed almost no correlation with traditional gold markets (such as the GLD ETF). Instead, tokenized gold volumes were driven by idiosyncratic crypto liquidity cycles. However, a structural shift began in the second quarter of 2025.

For the first time, tokenized gold volumes began to show a strong correlation (greater than 0.70) with traditional gold mining stocks and spot gold ETFs. By the first quarter of 2026, this correlation remained steady, suggesting that the on-chain gold market is finally beginning to respond to the same macro signals—such as inflation data, geopolitical risk, and interest rate changes—that drive the traditional commodity markets. As liquidity deepens, this convergence is expected to spread to other asset classes, allowing institutional desks to apply existing risk models and hedging strategies to their tokenized positions.

Broader Implications and the Institutional Imperative

The growth of the RWA sector signals that the financial industry is moving beyond the "pilot program" phase. Major players are no longer simply testing the technology; they are integrating it into their core distribution channels. The implications of this shift are profound for the future of global finance.

First, the rise of RWAs democratizes access to high-quality assets. By fractionalizing expensive assets like commercial real estate or private credit, blockchain technology allows a broader range of investors to access markets that were previously reserved for the ultra-wealthy or large institutional funds. Second, the move to on-chain rails significantly reduces settlement risk. In a T+0 (near-instant) settlement environment, the need for extensive collateral and the risk of counterparty default during the settlement window are virtually eliminated.

Finally, the transparency of the blockchain provides a level of auditability that legacy systems cannot match. Regulators and risk managers can monitor systemic risks in real-time, potentially preventing the kind of opaque contagion that has triggered financial crises in the past.

For traditional financial institutions, the message is clear: the transition to digital rails is no longer a matter of "if" but "how." The rapid scaling of the RWA market suggests that those who successfully integrate these technologies into their core offerings will capture significant market share in the coming decade. As the lines between traditional finance and digital assets continue to blur, the "New Rails" are being laid, creating a more efficient, transparent, and accessible global financial system.