The global financial landscape is undergoing a structural transformation as digital assets migrate from the periphery of the economy to its very core. While much of the initial discourse surrounding blockchain technology focused on the selection of specific protocols—prioritizing metrics such as transaction speed, cost efficiency, and contagion risk—the industry is now entering a secondary, more mature phase of development. This phase is defined not just by where assets are built, but by how they are monitored. As traditional financial institutions (TradFi) integrate with decentralized networks, the concept of on-chain transparency has shifted from a theoretical benefit to a non-negotiable regulatory baseline.

The maturation of the digital asset ecosystem is most visible in the rigorous compliance frameworks now being adopted by global organizations. According to recent industry benchmarks, the standards for monitoring illicit financial flows have tightened so significantly that the average compliance posture expected in 2026 was considered the "gold standard" or top-decile performance as recently as 2020. This rapid evolution reflects a broader trend: the "new rails" of finance are being built with surveillance and compliance as foundational components, rather than afterthoughts.

The Evolution of Compliance: A New Industry Benchmark

To quantify the progress made in digital asset oversight, analysts have developed a "compliance index" that aggregates several key performance indicators. This index considers alert severity, trigger sensitivity, and minimum dollar-detection floors to measure how strictly an organization configures its monitoring for indirect illicit exposure. By benchmarking current organizations against the 90th percentile of strictness observed in 2020, a clear trajectory of professionalization emerges.

In 2020 and 2021, the industry was still grappling with the nuances of on-chain monitoring. During this period, only approximately 10% of newly onboarded organizations met what is now defined as the "gold standard" for alerting. However, a significant inflection point occurred in 2023, as regulatory clarity began to emerge in major jurisdictions. By 2026, data suggests that nearly half of all newly onboarded organizations operate at or above the elite alerting standards of five years ago.

This shift indicates that the baseline for entry into the digital asset space has risen. Financial institutions joining the ecosystem today are not entering a "Wild West" environment; they are joining a sophisticated infrastructure where standard configurations would have been considered industry-leading in the previous decade.

The Divergence Between Traditional Finance and Crypto-Native Entities

A critical finding in the maturation of the market is the widening gap between the compliance postures of traditional financial institutions and crypto-native exchanges. TradFi entities, accustomed to decades of stringent oversight from bodies such as the Financial Action Task Force (FATF) and national regulators like FinCEN or the FCA, exhibit a significantly lower tolerance for suspicious flows.

The disparity is most evident in the detection thresholds set by these two groups. Traditional financial institutions typically implement alerting thresholds that are two to five times tighter than those of their crypto-native counterparts. For indirect exposure to non-illicit but suspicious fund flows, crypto exchanges set an average alerting minimum of $950. In contrast, traditional financial institutions set their floor at just $150.

The gap narrows when examining direct illicit exposure, where both sectors demonstrate high levels of caution. For direct flows from known illicit sources, crypto exchanges generally trigger alerts at the $100 mark, while traditional financial institutions maintain a stricter threshold of $55. This heightened sensitivity in TradFi is largely a byproduct of legacy regulatory expectations, where even minor lapses in anti-money laundering (AML) protocols can result in multi-billion dollar fines and severe reputational damage.

Understanding Direct vs. Indirect Exposure

To navigate the complexities of on-chain compliance, it is essential to distinguish between direct and indirect exposure. Direct exposure occurs when funds arrive at an institution immediately from a known illicit source, such as a sanctioned wallet or a darknet market. Monitoring for direct exposure has become a standardized practice globally, with little variation in how institutions handle these "first-hop" transactions.

Indirect exposure, however, remains a point of significant ambiguity and strategic importance. It refers to funds that pass through one or more intermediary addresses—often referred to as "hops"—before reaching the final destination. In the world of decentralized finance, illicit actors utilize "layering" techniques, creating multiple private wallets to move funds with minimal friction. This process is designed to obfuscate the origin of the assets.

While direct monitoring is a baseline requirement, the industry is currently debating how aggressively to flag funds that touched an illicit source several hops back. If a compliance program is too lenient with indirect exposure, it risks allowing laundered funds to enter the legitimate financial system. Conversely, if a program is too aggressive, it may result in a high volume of "false positives," overwhelming compliance teams and disrupting legitimate commerce.

Categorical Sensitivity and Zero-Tolerance Thresholds

Analysis of detection thresholds across dozens of illicit categories reveals a hierarchy of risk. Global compliance teams have identified certain categories that carry such high regulatory and reputational stakes that they necessitate a "zero-tolerance" approach.

For the most sensitive categories—including child abuse material (CSAM), sanctioned entities, terrorist financing, and special measures—organizations across the board set alerting thresholds at the lowest possible denomination, often as little as one penny. In these instances, the distinction between direct and indirect exposure effectively vanishes; any connection to these activities, regardless of how many hops away, triggers an immediate investigation.

For other categories, such as ransomware, fraud shops, scams, and darknet markets, the gap between direct and indirect thresholds is more pronounced. In many cases, indirect thresholds are set 10 to 20 times higher than direct equivalents. For instance, an institution might alert on $10 of direct ransomware exposure but ignore indirect exposure until it surpasses $100. Illicit actors are keenly aware of these discrepancies and often design their laundering strategies to stay just below these indirect detection floors.

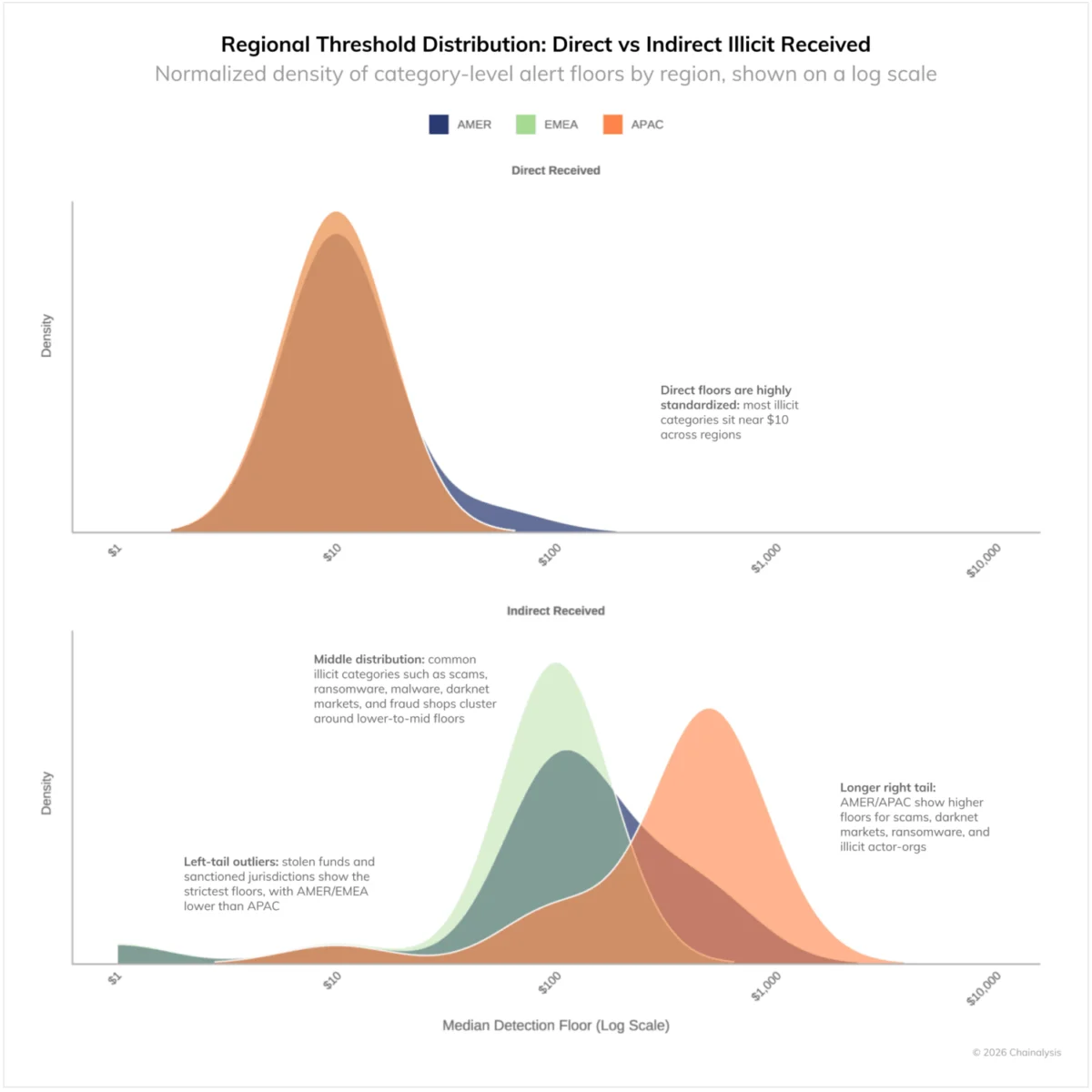

Regional Variations in Regulatory Landscapes

While the technology behind digital assets is global, the compliance programs monitoring them are deeply influenced by regional legal frameworks. Data comparing the Americas (AMER), Europe, the Middle East, and Africa (EMEA), and the Asia-Pacific (APAC) regions shows a marked divergence in indirect monitoring standards.

- EMEA (Europe, Middle East, and Africa): This region maintains the strictest and most concentrated compliance distributions. Driven largely by the European Union’s Markets in Crypto-Assets (MiCA) regulation and strict AML directives, organizations in EMEA set low alerting thresholds—often around $100—for categories like scams and ransomware.

- AMER (Americas): The Americas occupy a middle ground. While the region shares a zero-tolerance tail with EMEA for sanctions and stolen funds, it exhibits more leniency in other categories. The distribution in the U.S. and surrounding markets shows a broader dispersion, reflecting a regulatory environment that is still evolving through enforcement actions and judicial rulings.

- APAC (Asia-Pacific): This region demonstrates the most lenient configurations. The distribution of alerting thresholds is right-skewed, with secondary clustering at much higher dollar values. This suggests a more heterogeneous regulatory landscape where different jurisdictions within the region have vastly different expectations for indirect monitoring.

For global financial institutions, these regional differences are a critical consideration for due diligence. A counterparty headquartered in an APAC jurisdiction may be operating under significantly more relaxed monitoring standards than one in EMEA, even if both utilize the same underlying compliance software.

Implications for the Future of Institutional Finance

The professionalization of on-chain monitoring has profound implications for the future of the financial industry. As digital assets continue to reshape the "rails" of finance, several key trends are likely to emerge:

Compliance as a Competitive Advantage

In an era where institutional capital demands "regulatory defensibility," the rigor of an organization’s monitoring configuration is becoming a core value proposition. Institutions that can demonstrate superior oversight of indirect risk will be better positioned to attract Tier-1 partners and navigate the complexities of cross-border digital trade.

The Rise of Real-Time Investigative Workflows

The shift from reactive remediation to proactive investigation is accelerating. Tools that provide real-time transaction monitoring and complex fund-flow tracing are no longer optional. The ability to identify a suspicious pattern before the funds are "off-ramped" or converted is the new benchmark for excellence in financial crime prevention.

Standardization of Indirect Risk

While ambiguity currently exists regarding indirect exposure, the industry is moving toward a more standardized approach. As regulators become more sophisticated in their understanding of blockchain analytics, they are likely to issue clearer guidance on "how many hops is too many," eventually narrowing the gap between direct and indirect monitoring thresholds.

Integration of Tokenized Real-World Assets (RWAs)

As traditional assets like bonds, real estate, and private equity are tokenized, the need for stringent compliance will only grow. The "New Rails" must be able to handle the high-velocity nature of digital assets while maintaining the integrity of the multi-trillion dollar markets they represent.

The transition to digital-asset-based finance is not merely a technological upgrade; it is a fundamental shift in how risk is managed. The data confirms that the industry is rapidly maturing, moving away from the experimental phase and toward a disciplined, institutional-grade ecosystem. For financial institutions, the message is clear: selecting the right blockchain is only the beginning. The real challenge—and the real opportunity—lies in the sophisticated monitoring of the assets that flow across it.