The global financial landscape is currently undergoing a structural transformation as digital assets migrate from the periphery of speculative trading into the core infrastructure of traditional finance. This shift, often described as the construction of "new rails" for value transfer, requires more than just high-performance blockchains; it demands a sophisticated, transparent, and rigorous compliance framework capable of meeting the stringent requirements of global regulators. As traditional financial institutions (TradFi) increasingly adopt tokenization and decentralized ledgers, the focus has shifted from the technical capabilities of the underlying chains—such as speed and cost—to the integrity of the transactions occurring upon them. According to recent industry benchmarks and data from Chainalysis, the standards for on-chain monitoring have matured at an unprecedented rate, with today’s average compliance configurations surpassing what was considered the "gold standard" only a few years ago.

The Maturation of On-Chain Compliance: 2020 to 2026

To understand the current state of digital asset compliance, it is necessary to examine the trajectory of the industry over the last half-decade. In 2020, the decentralized finance (DeFi) "summer" sparked a massive influx of capital and complexity into the blockchain ecosystem. At that time, compliance norms were still in their infancy. Most organizations focused almost exclusively on direct exposure—identifying funds coming immediately from known illicit sources. Indirect exposure, or the monitoring of funds that have passed through multiple intermediary "hops" before reaching an institution, was an emerging concept with few standardized rules.

A "compliance index" developed to measure alert severity, trigger sensitivity, and minimum dollar-detection floors reveals a stark evolution. In 2020 and 2021, only approximately 10% of newly onboarded organizations met the high-stringency threshold that was then considered the industry’s gold standard. However, by 2023, the industry reached an inflection point. As regulatory bodies like the Financial Action Task Force (FATF) and the European Union began clarifying their expectations for virtual asset service providers (VASPs), the baseline for acceptable monitoring rose significantly. Projections for 2026 suggest that nearly half of all newly onboarded organizations will operate at or above the 2020 gold standard. This represents a rapid professionalization of the ecosystem, signaling that the infrastructure is now robust enough to support large-scale institutional participation.

Understanding the Complexity of Direct vs. Indirect Exposure

The core challenge for compliance teams in the digital asset space lies in the distinction between direct and indirect exposure. Direct exposure occurs when a transaction involves a known illicit wallet, such as a sanctioned entity or a darknet market, in a single hop. Monitoring this is now a standardized industry requirement, akin to traditional anti-money laundering (AML) checks.

Indirect exposure, however, is where the complexity—and the risk—resides. Because blockchain technology allows for the rapid creation of private wallets and the "layering" of transactions, illicit actors often move funds through several intermediary addresses to obscure their origin. In traditional finance, this layering process is slowed by the need to pass "Know Your Customer" (KYC) checks at every institution. On-chain, this can happen in seconds.

The industry remains divided on how aggressively to flag these indirect flows. If a compliance team sets its "Know Your Transaction" (KYT) alerts too high, they risk being overwhelmed by "false positives"—legitimate transactions that happen to have touched a suspicious source many hops ago. If they set them too low, they risk missing sophisticated money laundering schemes. The current trend shows that institutions are increasingly opting for tighter thresholds, prioritizing regulatory safety over operational convenience.

The Compliance Gap: Traditional Finance vs. Crypto-Native Exchanges

One of the most significant findings in the recent analysis of compliance behavior is the widening gap between traditional financial institutions and crypto-native exchanges. TradFi entities, which operate under a legacy of heavy regulation and "zero-fail" compliance cultures, exhibit a much lower tolerance for suspicious flows.

The data shows that traditional financial institutions set their alerting thresholds two to five times tighter than their crypto-native counterparts. For indirect exposure to non-illicit flows (which may still carry risk profiles), crypto exchanges set an average alerting floor at $950. In contrast, traditional financial institutions set that same floor at just $150.

When it comes to illicit funds, the gap narrows but remains telling. Crypto exchanges generally trigger alerts for illicit flows starting at $100, while financial institutions have lowered their threshold to $55. This heightened sensitivity reflects the "reputational contagion" risk that traditional banks face. For a global bank, even a small transaction linked to a sanctioned jurisdiction can result in massive fines and a loss of public trust, whereas crypto-native exchanges have historically operated with a higher risk appetite.

Category-Specific Sensitivity and the Zero-Tolerance Mandate

Not all illicit categories are treated equally by compliance algorithms. Organizations across the board exhibit a near "zero-tolerance" policy for the most severe categories of crime. For transactions linked to child abuse material (CSAM), terrorist financing, sanctioned entities, and special measures, the alerting threshold is frequently set at one penny. This reflects a global consensus that any association with these activities—direct or indirect—is an existential risk to the organization.

For other categories, such as ransomware, fraud shops, and darknet markets, there is more variance. Indirect thresholds for these categories often run 10 to 20 times higher than direct thresholds. For instance, an institution might alert on a $10 direct transaction from a ransomware group but wait until the amount reaches $100 if the funds have passed through several intermediary wallets. This discrepancy is a known vulnerability; illicit actors are aware of these "detection floors" and often design their laundering strategies to stay just beneath the thresholds of the most common compliance software configurations.

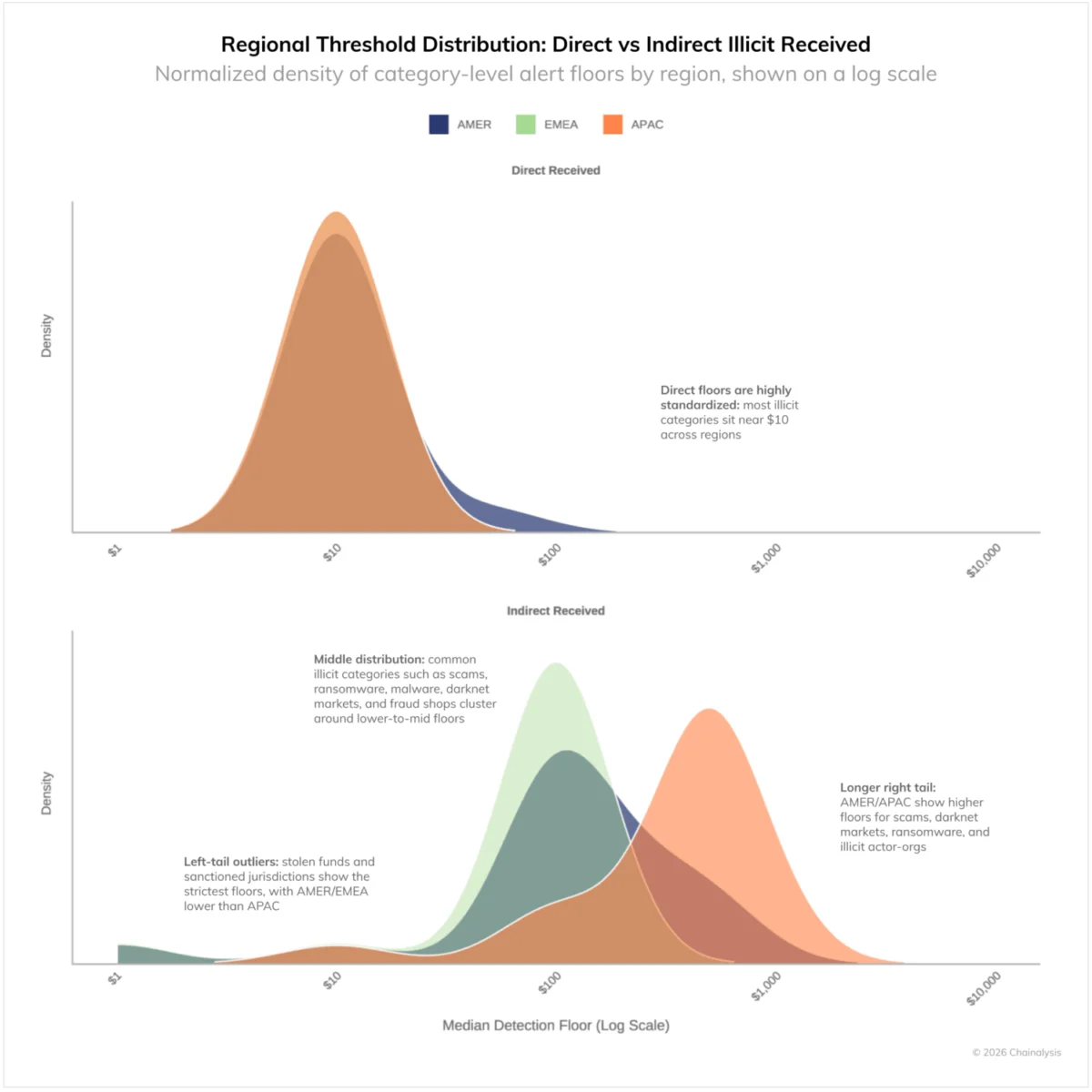

Regional Divergence: EMEA, AMER, and APAC

Geography plays a pivotal role in how compliance programs are structured, driven largely by the local legal and regulatory environment. While direct exposure monitoring is globally uniform—regulators in every jurisdiction expect institutions to catch direct hits—indirect monitoring varies significantly by region.

- EMEA (Europe, Middle East, and Africa): This region maintains the strictest and most concentrated compliance distributions. Driven by the European Union’s rigorous AML directives and the upcoming Markets in Crypto-Assets (MiCA) regulation, organizations in EMEA set low alerting thresholds (around $100) across almost all illicit categories. The region shows a strong preference for zero-tolerance policies regarding stolen funds and sanctioned jurisdictions.

- AMER (The Americas): The Americas region, dominated by the United States’ regulatory landscape, falls in the middle. It shares the zero-tolerance tail of EMEA for high-risk categories but shows more leniency in other areas. The distribution of thresholds in AMER is broader, reflecting a diverse mix of institutional risk appetites and a regulatory environment that is still in the process of finalizing certain on-chain standards.

- APAC (Asia-Pacific): The APAC region exhibits the most lenient configurations and the widest dispersion of thresholds. This is likely due to the heterogeneous nature of the region’s regulatory frameworks, which range from the strict prohibitions in some countries to more permissive environments in others. Institutions in APAC often set higher dollar-value triggers for indirect alerts, which may present a higher risk of undetected layering for global counterparties.

Implications for the Future of Institutional Digital Assets

The evolution of these "new rails" suggests that the future of finance will be defined by "regulatory defensibility." As institutional capital continues to flow into digital assets, the ability to prove a rigorous compliance posture is becoming a competitive advantage.

Financial institutions entering the space must recognize that simply having compliance software is no longer sufficient. The configuration of that software—how the "knobs and dials" are turned—is what regulators will scrutinize. An institution using 2020-era settings in a 2026 environment will likely be viewed as non-compliant, even if they are using the same basic tools as their peers.

Furthermore, the regional divergence in monitoring standards highlights the necessity of deep due diligence when engaging in cross-border partnerships. A counterparty headquartered in a region with more lenient indirect monitoring may unknowingly be passing on "tainted" liquidity to a partner in a stricter jurisdiction.

In conclusion, the foundations of finance are indeed being reshaped by digital assets, but this transformation is not merely technical. It is a fundamental shift in how risk is measured and mitigated. As the industry moves toward a more standardized, high-stringency compliance model, the transparency of the blockchain—once feared by institutions—is proving to be its greatest asset, providing a level of auditability and security that traditional "closed" financial systems can rarely match. The "new rails" are being built with compliance at their core, ensuring that the digital financial system of the future is as secure as it is efficient.