The tokenization of Real World Assets (RWAs) has transitioned from a speculative technological experiment into a foundational pillar of modern traditional finance (TradFi). As global banks, sovereign wealth funds, and asset managers move beyond the era of isolated pilot programs toward live, large-scale deployments, they are confronting a fundamental infrastructure dilemma: the selection of the underlying blockchain architecture. This choice is no longer merely a technical preference but a strategic decision that impacts profit and loss, regulatory compliance, and systemic risk. According to new research from Chainalysis, the "perfect" general-purpose blockchain does not exist; instead, the industry is witnessing a landscape defined by critical trade-offs across five primary axes: speed, cost volatility, contagion risk, illicit exposure, and governance.

The Institutional Shift Toward On-Chain Finance

For years, the promise of tokenization was centered on theoretical efficiencies—fractional ownership, 24/7 markets, and reduced settlement times. However, the current cycle has seen these theories materialize into multi-billion-dollar products. The core of this shift lies in "The New Rails," a digital infrastructure that allows traditional assets such as US Treasuries, corporate bonds, and private equity to be represented as tokens on a distributed ledger.

The move toward these rails is driven by the necessity to modernize aging financial systems. Traditional settlement systems often rely on a complex web of intermediaries, leading to T+2 or T+1 settlement cycles and significant capital lock-ups. By moving these assets on-chain, institutions aim for atomic settlement—where the exchange of the asset and the payment occurs simultaneously and near-instantly. Yet, as institutions prepare for this transition, they must evaluate which "rail" suits their specific needs. The data suggests that networks are bifurcating into three distinct archetypes: Institutional Anchors, the Goldilocks sweet spot, and High-Frequency Engines.

A Chronology of Infrastructure Evolution

The path to the current infrastructure landscape began in earnest with the 2017-2018 Initial Coin Offering (ICO) boom, which primarily utilized Ethereum as a platform for speculative tokens. This was followed by the "DeFi Summer" of 2020, which tested the limits of network throughput and transaction costs. By 2022, the collapse of centralized entities like FTX highlighted the dangers of systemic dependency and the need for more transparent, decentralized governance.

In 2024 and early 2025, the narrative shifted toward institutional-grade RWAs. BlackRock’s launch of the BUIDL fund on Ethereum marked a watershed moment, signaling that the world’s largest asset manager viewed public blockchains as viable for institutional products. Subsequently, Franklin Templeton’s expansion of its OnChain US Government Money Fund (FOBXX) to networks like Solana and Polygon further illustrated the industry’s multi-chain trajectory. This evolution has led to the current state where the choice of blockchain is dictated by the specific risk profile and performance requirements of the asset being tokenized.

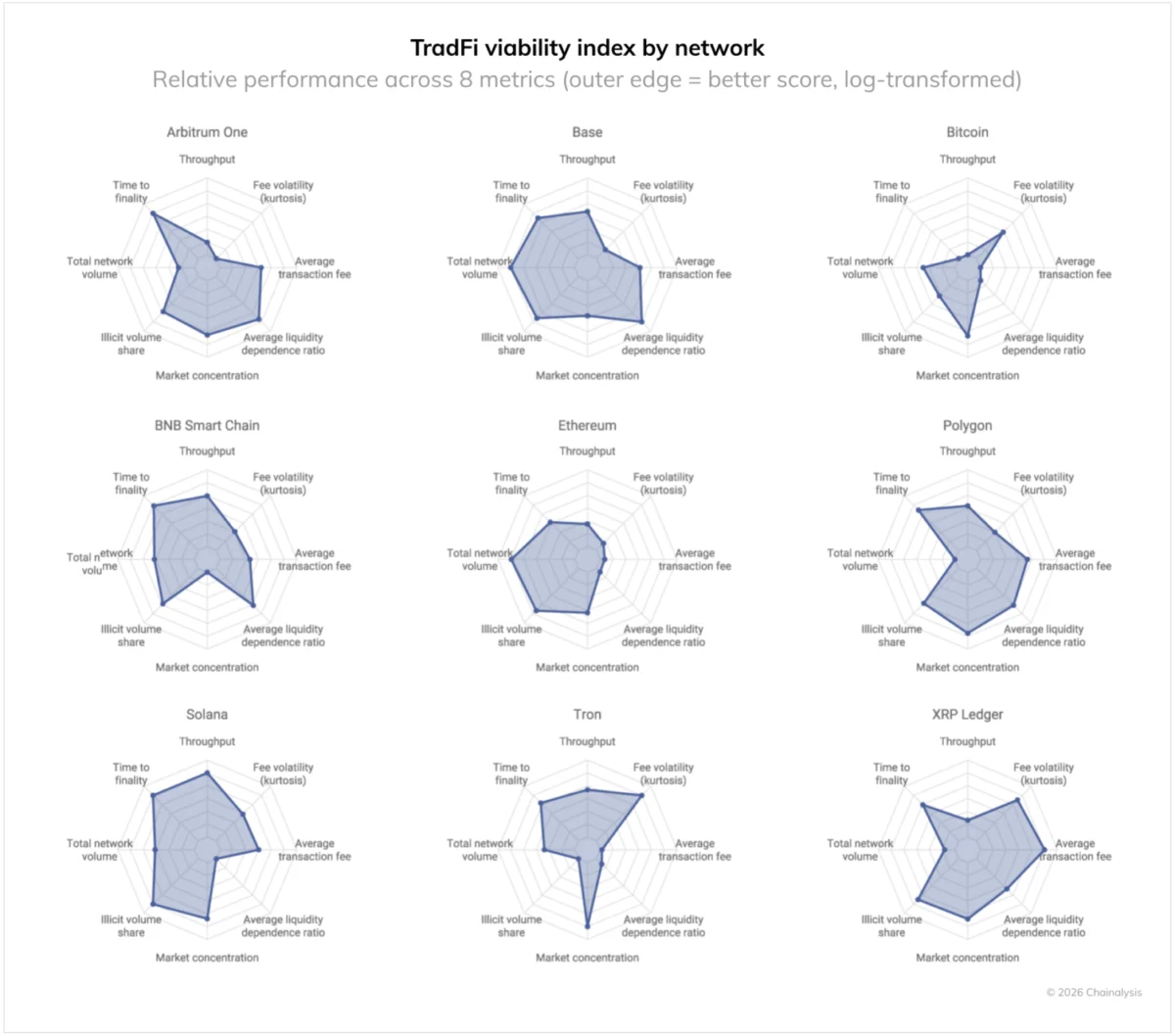

Operational Costs and the Statistical Analysis of Fee Predictability

For a financial institution, the absolute cost of a transaction is often less important than the predictability of that cost. To quantify this, analysts use "kurtosis"—a statistical measure of "tail risk." A high kurtosis score indicates that a network is prone to sudden, violent pricing shocks during periods of congestion, which can disrupt automated settlement processes and internal budgeting.

Data tracking daily average network fees since April 2024 reveals a stark contrast between networks. Bitcoin, for instance, exhibits extreme tail risk with a kurtosis score of 246. This volatility is largely attributed to the rise of protocols like Runes and Ordinals, which allow users to inscribe data directly onto the blockchain. These activities often trigger surges in network demand that are unrelated to financial settlement, causing fees to spike from a few dollars to hundreds of dollars in a matter of hours.

Conversely, TRON has emerged as a model of fee stability with a kurtosis score of nearly zero. Its tightly clumped fee distribution explains its dominance in the global stablecoin payment market, particularly in emerging economies where fee predictability is paramount. Ethereum, following its Dencun upgrade, has also achieved a significant degree of stability by offloading data to Layer-2 (L2) networks, effectively shielding the Mainnet from the extreme "gas wars" of previous cycles.

The Throughput vs. Finality Paradox

When evaluating network speed, financial institutions must distinguish between raw throughput (transactions per second or TPS) and time to finality (the time it takes for a transaction to be irreversible).

Solana remains the undisputed leader in raw throughput, processing more than twice the on-chain volume of its nearest competitor, TRON. This makes Solana the preferred choice for high-frequency trading applications and retail-facing products that require a seamless, instant user experience. Franklin Templeton’s decision to utilize Solana for its FOBXX fund was explicitly linked to the network’s high-throughput, monolithic architecture, which the firm noted has matured significantly despite past technical challenges.

However, throughput is only half of the equation. For high-value institutional settlements, "hard finality" is the critical metric. Arbitrum has consistently held the top spot for the fastest time to finality among Layer-2 networks. While Layer-2s offer "soft finality" (instant confirmation at the L2 level), they still face "L1 processing risk." This refers to the time it takes for the L2 to batch and finalize transactions on the Ethereum Mainnet, a process that can take anywhere from 15 minutes to several hours. For a transaction involving millions of dollars, the difference between soft and hard finality can represent a significant window of counterparty risk.

Contagion Risk and Institutional Dependency

The 2022 crypto contagion served as a stark reminder of how interconnected digital asset markets are. To measure systemic risk, Chainalysis monitors "centralized exchange (CEX) dependency"—the ratio of direct inter-exchange liquidity transfers to an exchange’s on-chain liabilities.

Solana’s history provides a cautionary tale. Prior to the FTX collapse, the network exhibited excessively high interconnectivity between exchanges, which primed the ecosystem for a rapid collapse when a major player failed. While Solana has since rebounded to a 60% institutional dependency, it remains more volatile in this regard than older networks like Bitcoin and Ethereum. These "Institutional Anchors" typically maintain dependency ratios below 50%, suggesting a more resilient and decentralized liquidity base that is less prone to the "bank run" dynamics seen in newer ecosystems.

The Compliance Mandate: Navigating Illicit Exposure

For regulated entities, compliance is not optional; it is a prerequisite for market entry. A key metric in this space is the "Green Zone"—the quadrant where high liquidity meets low illicit exposure.

Ethereum, Solana, and Base currently sit in this TradFi sweet spot. These networks handle trillions of dollars in volume while maintaining an illicit activity share of less than 1%. BlackRock’s BUIDL fund, which has become the largest tokenized money market fund by assets under management (AUM), was first deployed on Ethereum specifically because of this balance of deep liquidity and a manageable compliance profile.

In contrast, TRON presents a more complex case. While it possesses massive institutional-scale liquidity—acting as the primary rail for global stablecoin OTC desks—its proportion of illicit service inflow approaches 4%. This does not necessarily disqualify the network for institutional use, but it does necessitate more robust real-time monitoring and compliance tools, such as Know Your Transaction (KYT) and address screening solutions, to mitigate risk.

Governance and Crisis Management

The final, and perhaps most qualitative, trade-off involves governance. Financial institutions must decide between the "code is law" immutability of Bitcoin and the more interventionist governance structures of Proof of Stake (PoS) ecosystems.

In the event of a catastrophic hack or a systemic failure, the existence of an oversight authority can be a vital safeguard. For example, the Arbitrum Security Council and various Decentralized Autonomous Organizations (DAOs) have the theoretical power to pause protocols or reverse transactions under extreme circumstances. For a traditional bank, the ability to "call someone" during a crisis is often a legal or risk-management requirement, making governed L2s more attractive than purely immutable chains.

Market Implications and the Path Forward

The data indicates that the future of finance will not be built on a single blockchain but on a fragmented yet interoperable multi-chain ecosystem. The choice of architecture is increasingly being dictated by the asset class:

- Tokenized Bonds and Securities: These assets prioritize settlement finality and regulatory auditability. Ethereum Mainnet remains the gold standard for these use cases, as evidenced by Société Générale’s Forge platform.

- High-Frequency Trading and Retail Payments: These require low costs and high throughput, favoring Solana or high-performance L2s like Arbitrum and Base.

- Global Stablecoin Settlement: For cross-border payments where fee predictability is the primary concern, TRON continues to hold a significant market share.

BlackRock CEO Larry Fink has been vocal about this transition, stating that tokenization represents "the next major evolution in market infrastructure." Fink’s ambition to tokenize "all assets," especially those with multiple levels of intermediaries, suggests a future where the entire financial stack—from the underlying asset to the payment rail—operates on-chain.

As stablecoin volume is projected to reach $1.5 quadrillion by 2035, the infrastructure decisions made by financial institutions today are no longer technical experiments; they are existential strategic moves. By utilizing on-chain data to map the trade-offs of speed, cost, risk, and compliance, institutions can bypass the hype and build on the rails that will support the next century of global finance. The era of pilot programs is over; the era of the on-chain financial economy has begun.