The transition of the Ethereum network from a Proof-of-Work (PoW) consensus mechanism to Proof-of-Stake (PoS), a monumental event known as "The Merge," has triggered a seismic shift in the cryptocurrency mining landscape, resulting in a total collapse of profitability for graphics card-based operations. For nearly a decade, Ethereum served as the primary economic engine for GPU miners worldwide, offering a lucrative and relatively stable return on investment for hardware. However, following the successful implementation of The Merge on September 15, 2022, the vast computational power once dedicated to Ethereum has flooded into smaller PoW networks, driving mining difficulty to unsustainable levels and pushing daily returns into negative territory for the majority of participants.

The Great Migration and the Hashrate Overload

Before The Merge, Ethereum’s hashrate—the total computational power securing the network—consistently hovered between 850 and 900 Terahashes per second (TH/s). In contrast, the secondary markets for GPU mining, such as Ethereum Classic (ETC), Ravencoin (RVN), Ergo (ERGO), and Flux, possessed hashrates that were orders of magnitude smaller. For example, Ethereum Classic typically operated with a hashrate of around 25 to 30 TH/s.

When Ethereum officially switched to PoS, miners were faced with a binary choice: liquidate their hardware or point their rigs toward these alternative coins. The result was an immediate and overwhelming migration of "orphan" hashrate. Within 48 hours of The Merge, the hashrate of Ethereum Classic surged by nearly 500%, peaking at over 300 TH/s. While this surge technically improved the security of the ETC network, it created a catastrophic economic environment for individual miners.

Cryptocurrency networks utilize an automated mechanism known as "mining difficulty" to ensure that blocks are found at a consistent interval regardless of how many miners are active. As the hashrate on networks like ETC and Ravencoin skyrocketed, the difficulty adjusted upward almost instantly. With more miners competing for the same limited number of daily block rewards, the "slice of the pie" for each individual miner shrank to a fraction of its former size.

Analyzing the Data: The Reality of Negative Profits

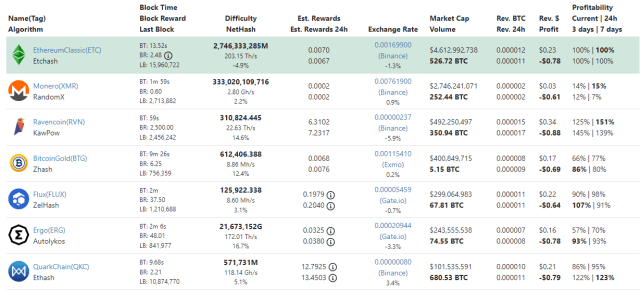

Data from industry-standard mining calculators, such as WhatToMine, paints a grim picture for the post-Merge mining economy. Under current conditions, the cost of electricity required to run high-performance graphics cards now exceeds the value of the cryptocurrency those cards can generate.

For a standard mining configuration utilizing three AMD RX 480 graphics cards—a staple of the mid-range mining community—the daily profit currently sits at approximately -$0.78 per hour, assuming a global average electricity cost of $0.10 per kilowatt-hour (kWh). Even for miners utilizing top-tier, high-efficiency hardware like the NVIDIA GeForce RTX 3090 Ti, the numbers remain firmly in the red, with hourly losses averaging -$0.50.

These calculations do not account for the additional overhead costs such as cooling, hardware maintenance, or the initial capital expenditure (CAPEX) required to purchase the rigs. In regions with higher energy costs, such as parts of Europe and the United Kingdom where prices have recently spiked above $0.30 per kWh, the losses are even more pronounced, effectively making GPU mining a "pay-to-play" hobby rather than a viable business model.

Chronology of the Mining Collapse

The journey toward this profitability crisis began years ago but accelerated rapidly in the final months of 2022:

- Late 2020 – Mid 2022: The "Golden Age" of GPU mining. Ethereum prices soared, and the EIP-1559 upgrade, while burning some fees, did not significantly dampen miner enthusiasm. Hardware prices for GPUs reached 3x MSRP as demand outstripped supply.

- August 2022: Ethereum developers confirmed the firm date for The Merge. Speculative mining began on "Merge-resistant" forks like ETHW (EthereumPoW), but market interest remained low.

- September 15, 2022: The Merge occurred at 06:42:42 UTC. Ethereum ceased to be a PoW chain. Tens of millions of GPUs worldwide were suddenly "unemployed."

- September 16–20, 2022: The "Hashrate War" ensued. Miners cycled through various coins—ETC, RVN, ERGO, FLUX, and Beam—searching for profitability. Each time a coin showed a glimmer of profit, a wave of hashrate followed, driving the difficulty up and the profit back down.

- October 2022 and Beyond: The market entered a period of "miner capitulation." Large-scale mining farms began shutting down operations, and the secondary market for used GPUs became flooded with inventory, leading to a crash in hardware resale values.

Industry Reactions and Market Sentiment

The reaction from the mining community has been a mixture of frustration, resignation, and a desperate search for "the next big thing." Leading mining pool operators, such as F2Pool and Ethermine, were forced to pivot their business models. Ethermine, once the largest Ethereum mining pool, launched a staking service to accommodate the new PoS reality, effectively signaling the end of their PoW-centric era.

Many small-scale miners have taken to social media and community forums to express their disappointment. "We knew The Merge was coming, but I don’t think anyone realized how quickly the secondary coins would become unprofitable," noted one long-time miner on Reddit. "It’s not just that profits are low; they are literally non-existent. You are paying the power company more than you’re getting in crypto."

Hardware manufacturers like NVIDIA and AMD have also felt the ripple effects. During the mining boom, these companies saw record-breaking revenues from GPU sales. Post-Merge, both companies have had to adjust their financial forecasts as the "mining demand" vanished overnight. The sudden availability of cheap, used GPUs on sites like eBay has also cannibalized the sales of new, current-generation graphics cards.

The Broader Impact and Future Implications

The collapse of GPU mining profitability has several far-reaching implications for the blockchain industry and the environment:

1. Environmental Sustainability:

The most immediate positive impact of The Merge is the drastic reduction in global energy consumption. Ethereum’s transition to PoS reduced the network’s electricity usage by an estimated 99.95%. While some miners have moved to other PoW coins, the overall energy footprint of the crypto industry has still seen a net decrease, as many rigs have been powered down permanently due to unprofitability.

2. The End of the GPU Mining Era?

For years, "mining at home" was a gateway for many individuals to enter the cryptocurrency space. With current difficulty levels, this entry point has been effectively closed. Unless a new PoW coin emerges with a massive market cap and a high block reward—or unless there is a monumental bull run in existing altcoins like Ravencoin—the era of profitable GPU mining for the average consumer may be over.

3. Network Security Risks:

The extreme volatility in hashrate presents security risks for smaller PoW chains. While a surge in hashrate makes a network more secure against 51% attacks, the subsequent "capitulation" (where miners leave the network because they can’t pay their bills) can lead to a sudden drop in security. This "yo-yo" effect makes these networks less stable in the long term.

4. Shift to ASIC Mining:

While GPU mining is struggling, Bitcoin mining—which utilizes Application-Specific Integrated Circuits (ASICs)—remains the dominant form of PoW. The post-Merge landscape has reinforced the divide between "general-purpose" mining (GPUs) and "specialized" mining (ASICs). As GPU mining fades, the PoW sector is becoming increasingly industrialized and centralized around specialized hardware that cannot be easily repurposed for other tasks.

Conclusion: A Market in Search of Equilibrium

At the time of writing, the price of Ethereum remains volatile, hovering around $1,400, down roughly 6% over the past week. However, the price of ETH is now decoupled from the mining economy. The miners who once secured the network are now a legacy component of its history.

The current state of negative profitability is a clear signal that the market is oversupplied with computational power. In economic terms, an equilibrium must eventually be reached. This will likely occur through a "shakeout" phase: as more miners shut down their machines to avoid mounting losses, the total hashrate on networks like Ethereum Classic will begin to decline. Eventually, the difficulty will drop to a level where the remaining, most efficient miners—those with the cheapest electricity and the most advanced hardware—can return to a state of marginal profitability.

Until that equilibrium is found, the graphics card mining industry remains in a state of hibernation. For the millions of GPUs that once powered the second-largest blockchain in the world, the options are now limited: find a use in high-performance computing (HPC) and AI rendering, sit idle in a closet, or be sold to a gamer at a steep discount. The Merge did more than just change a line of code; it fundamentally rewrote the economics of an entire industry.