OpenAI has unveiled a significant expansion of ChatGPT’s capabilities, introducing a new personal finance feature that directly connects to users’ bank accounts to provide highly personalized financial advice. This marks a pivotal shift from the generic budgeting tips ChatGPT has offered for years – the familiar refrains of "track subscriptions," "automate savings," and "cook at home more" – to a dynamic, data-driven financial assistant. The new functionality is initially rolling out to ChatGPT Pro subscribers, priced at $200 per month, within the U.S. on both web and iOS platforms.

The Evolution of AI in Personal Finance

For a considerable period, artificial intelligence, including large language models like ChatGPT, has been touted as a potential disruptor in the financial sector. Early iterations of AI chatbots could offer broad strokes of financial wisdom, drawing from vast datasets of public information. However, the inherent limitation was their inability to access real-time, individual financial data, rendering much of their advice theoretical rather than actionable. Users often found themselves having to manually input their financial details, a time-consuming and often cumbersome process, to elicit any truly personalized recommendations. This created a demand for a more integrated and intelligent financial companion, a gap OpenAI is now aggressively seeking to fill.

The advent of this personalized finance feature represents a maturation of AI’s role in consumer finance. It moves beyond theoretical guidance to practical application, leveraging actual spending patterns, income streams, and liabilities to construct a comprehensive financial profile. This shift is not merely an upgrade; it signifies a strategic push by OpenAI to embed its AI models deeper into the critical, sensitive aspects of users’ daily lives, mirroring trends seen in other sectors like healthcare.

Deep Dive into the New Feature: How it Works

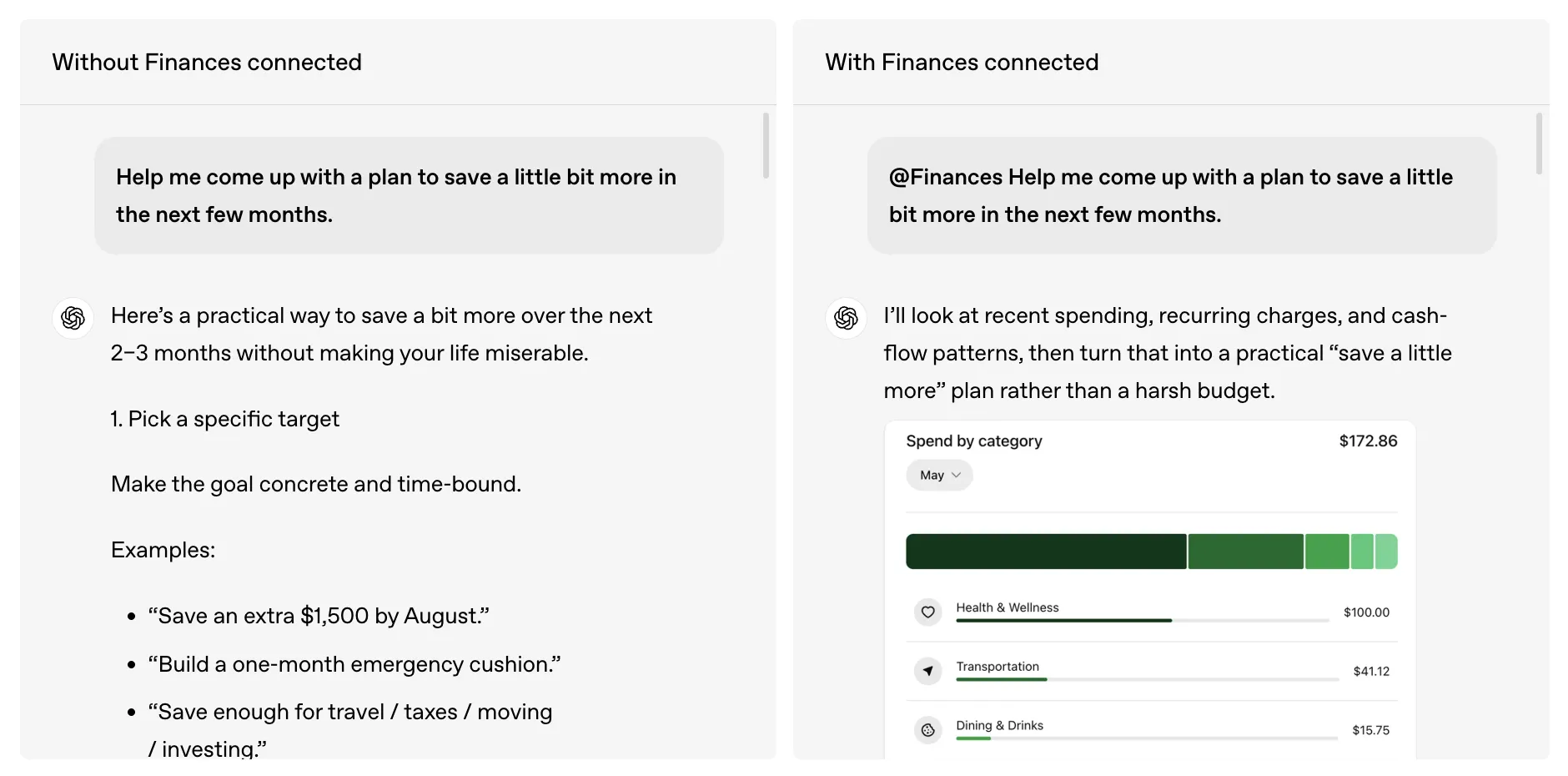

At the core of this innovative feature is its integration with Plaid, a leading financial data infrastructure provider. Plaid is already a ubiquitous presence in the fintech landscape, powering popular applications such as Venmo, Robinhood, and thousands of other digital financial services. By partnering with Plaid, ChatGPT gains secure, read-only access to a wide array of financial data from over 12,000 financial institutions across the United States. This extensive network includes major players like Chase, Fidelity, Schwab, American Express, and Capital One, ensuring broad compatibility for a vast majority of users.

Upon connecting their accounts, users grant ChatGPT access to their balances, transaction history, investment portfolios, and liabilities. This rich, real-time data allows the AI to move beyond generalized advice. For instance, a common prompt like "help me save more" would previously yield a standard list of suggestions: reducing subscriptions, cutting down on takeout, or automating transfers. With connected accounts, the AI can analyze a user’s actual spending over the last 90 days across specific categories like dining, shopping, and transportation. Based on this concrete data, it can then generate a personalized monthly savings plan, complete with real dollar targets tailored to the user’s specific financial habits and capacity.

Crucially, OpenAI emphasizes that this access is strictly read-only. The system cannot initiate transactions, move money between accounts, or access full account numbers. This limitation is designed to provide a layer of security and prevent unauthorized financial manipulation, addressing a primary concern for users entrusting sensitive data to an AI. The convenience factor is significant; what once required laborious downloading and uploading of bank statements is now an automated process, streamlining financial analysis for the end-user.

OpenAI’s Strategic Acquisitions and Development Timeline

This foray into personalized finance is not an impromptu venture but rather a carefully orchestrated strategic move by OpenAI. The company has been systematically acquiring specialized fintech startups, laying the groundwork for this advanced offering.

Just a month prior to this launch, in April, OpenAI acquired Hiro Finance. Hiro had positioned itself as an "AI personal CFO," offering advanced financial management solutions. The acquisition was effectively an "acqui-hire," absorbing Hiro’s talent and technology into OpenAI’s ecosystem while Hiro’s standalone product ceased operations. This move brought in crucial expertise and technology in personal financial management, accelerating OpenAI’s development timeline.

This wasn’t OpenAI’s first foray into fintech acquisitions. Less than a year before the Hiro deal, the company had acquired Roi, a startup specializing in personalized investing applications. These strategic pickups clearly indicate a deliberate and sustained effort by OpenAI to build out a robust financial services vertical within its AI platform, leveraging external innovations to enhance its core capabilities.

To validate the efficacy of its new financial model, OpenAI collaborated with over 50 finance professionals to develop and evaluate a comprehensive benchmark for complex personal finance tasks. The default model for the Finances feature, GPT-5.5 Thinking, achieved a score of 79 out of 100 on this rigorous benchmark. An even more advanced version, GPT-5.5 Pro, available exclusively to Pro subscribers, scored an impressive 82.5. These scores, while not a guarantee of perfection, provide a quantitative measure of the models’ proficiency in navigating intricate financial scenarios and generating accurate insights, offering a degree of confidence to potential users and industry observers.

The Broader Landscape of AI in Finance: Competition and User Trends

OpenAI is not operating in a vacuum. The race to integrate advanced AI into financial services is intensifying across the tech and fintech industries. Perplexity, another prominent AI company, recently launched its own Plaid-connected finance product, signaling a broader industry trend towards real-time, personalized financial assistance. Furthermore, Intuit, the financial software giant behind TurboTax and QuickBooks, is reportedly preparing its own integration with ChatGPT. This forthcoming collaboration promises to enable even more sophisticated functionalities, such as estimating the tax impact of selling stocks or predicting credit card approval odds, all accessible within the familiar chat interface. This burgeoning competitive landscape underscores the growing recognition of AI’s transformative potential in democratizing and streamlining financial management.

The impetus for these developments is rooted in demonstrable user behavior. OpenAI reports that over 200 million people already engage with ChatGPT monthly to ask financial questions. This staggering figure highlights a pre-existing demand for AI-driven financial insights, even if the tools available were previously rudimentary. The new feature, therefore, is not creating a new market but rather formalizing and significantly enhancing an interaction that is already widespread, offering a more sophisticated and relevant solution to an existing user base.

Addressing Key Concerns: Data Security and Fiduciary Duty

The introduction of a feature that connects an AI chatbot to sensitive financial accounts inevitably raises significant questions about data security and ethical responsibilities.

Data Security with Plaid:

OpenAI’s reliance on Plaid for financial data connectivity is a strategic choice, leveraging a well-established and highly secure infrastructure. Plaid employs bank-level encryption protocols to protect data in transit and at rest. Crucially, Plaid does not store users’ bank login credentials; instead, it uses encrypted tokens for ongoing access, minimizing the risk associated with direct credential storage. With a track record of processing over 150 million connections across more than 12,000 financial institutions without a single major breach, Plaid has built a reputation for robust security. This foundation provides a strong initial layer of protection for users’ financial information.

However, the real question extends beyond Plaid’s security to what happens once the data reaches OpenAI’s systems. OpenAI addresses this by stating that "Your conversations with connected financial accounts follow the same model training settings you choose across ChatGPT." This means if a user has opted out of contributing to model training, their financial conversations will also be excluded. Users retain the ability to disconnect their financial accounts at any time, and OpenAI commits to deleting synced data from its systems within 30 days of disconnection. These policies aim to offer users control over their data, though the broader implications of AI companies handling such sensitive information remain a topic of ongoing debate among privacy advocates and regulators.

The Fiduciary Question:

Perhaps the most critical distinction and potential point of contention lies in the legal and ethical responsibilities of this AI tool. OpenAI explicitly states that this feature "is not a financial advisor." This disclaimer is not merely semantic; it carries significant legal weight. A traditional financial advisor operates under a fiduciary duty, meaning they are legally obligated to act in their client’s best interest. This duty requires transparency, conflict-of-interest avoidance, and a commitment to providing advice that genuinely benefits the client, even if it means sacrificing personal gain.

ChatGPT, as an AI, has no such fiduciary duty. It can identify patterns, analyze spending, and suggest financial targets based on its algorithms and the data it accesses. However, it bears no legal responsibility for the outcomes of its advice. If a user makes a financial decision based on ChatGPT’s recommendations that leads to a loss, the liability rests solely with the user. This critical limitation contrasts sharply with the regulated environment of human financial advisory services. Regulators and financial institutions are likely to scrutinize this aspect closely, particularly as the product potentially expands beyond the niche market of Pro subscribers.

This approach mirrors OpenAI’s strategy in other sensitive domains, such as healthcare. Earlier this year, OpenAI launched a specialized ChatGPT for clinicians, offering tools to assist with clinical tasks. While the AI might "outperform humans" in certain diagnostic or informational contexts, OpenAI concurrently maintained that it did not claim responsibility for the clinical advice provided. This "playbook" of providing powerful, domain-specific AI tools without assuming direct liability for their recommendations appears to be a consistent strategy for the company as it ventures into highly regulated sectors.

Implications for the Future of Financial Advice

The launch of ChatGPT’s personalized finance feature carries profound implications for the future of financial advice, democratizing access to tailored financial planning while simultaneously posing new challenges.

Democratization of Financial Planning: Traditionally, highly personalized financial advice has been the preserve of wealthier individuals who can afford professional human advisors. This new AI tool has the potential to make sophisticated financial insights accessible to a much broader demographic, particularly those who might find traditional advisory services too expensive or intimidating. By providing actionable, data-driven advice at a relatively low cost (for Pro subscribers), ChatGPT could empower millions to better manage their finances, save more effectively, and plan for their financial futures.

Disruption of Traditional Advisory Services: While the AI explicitly states it’s not a financial advisor, its capabilities could disrupt segments of the traditional financial advisory market. For basic budgeting, savings planning, and analysis of spending habits, AI might offer a compelling, cost-effective alternative. Human advisors may need to pivot towards more complex financial planning, investment strategies requiring nuanced human judgment, emotional support during market volatility, and tax optimization that an AI, at its current stage, cannot fully replicate with fiduciary responsibility. The role of human advisors might evolve to become more focused on high-level strategy, complex problem-solving, and emotional coaching, complementing rather than being fully replaced by AI tools.

Challenges and Opportunities: The ethical considerations surrounding AI in finance are significant. Ensuring algorithmic fairness, preventing bias in recommendations, and continuously updating models to reflect dynamic economic conditions will be paramount. The potential for "robo-advisors" to exacerbate existing financial inequalities, if not carefully designed, is also a concern.

However, the opportunities are vast. Beyond personal budgeting, AI could assist in identifying optimal debt repayment strategies, analyzing investment portfolio performance against personal goals, or even providing initial guidance on retirement planning. For underserved populations, AI could offer a crucial first step towards financial literacy and empowerment. Regulatory bodies will face the task of developing frameworks that balance innovation with consumer protection, especially regarding liability, data privacy, and the definition of financial advice in the age of AI.

In conclusion, OpenAI’s new personal finance feature marks a significant leap in the integration of AI into daily financial management. By connecting directly to bank accounts via Plaid, ChatGPT can now offer unprecedented levels of personalized financial guidance, moving beyond generic advice to actionable, data-driven recommendations. This strategic expansion, bolstered by key acquisitions and rigorous benchmarking, reflects OpenAI’s commitment to embedding its AI models into critical life domains. While offering immense potential for democratizing financial planning and empowering users, the feature also brings into sharp focus critical questions surrounding data security, the absence of fiduciary duty, and the evolving landscape of financial advice in an AI-driven world. As this technology rolls out and evolves, its impact on individual finances and the broader financial industry will be closely watched.